L&T is well positioned to benefit from structural themes such as energy transition (green...

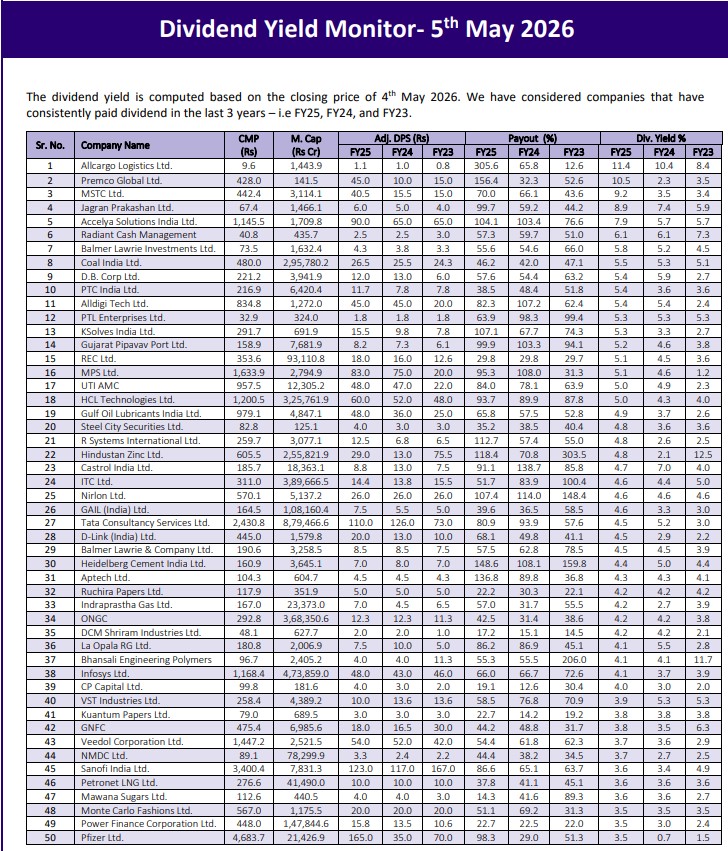

dividend yield is computed based on the closing price of 4th May 2026

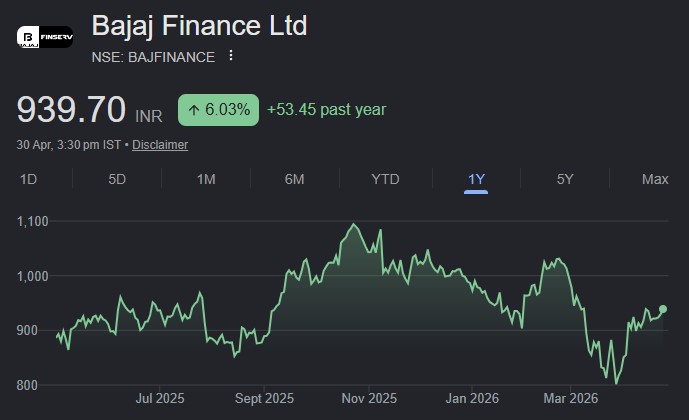

Lending franchises remain strong with Bajaj Finance AUM crossing ₹5 lakh crore (+22% YoY)...

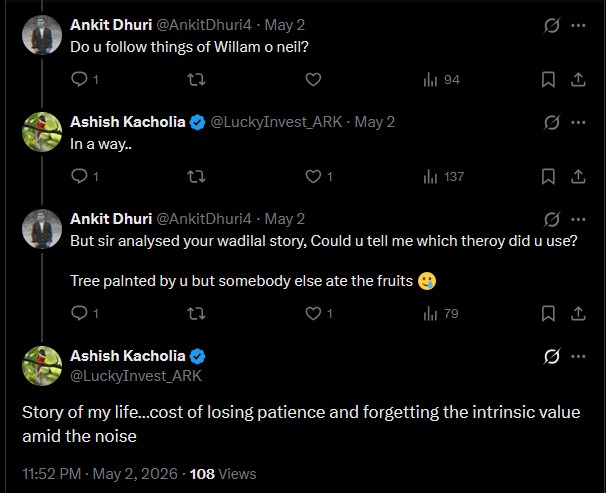

The "Vadilal Story" is a reminder that the stock market is a device for...

The company is strategically expanding its portfolio of services leveraging its knowhow of complex...

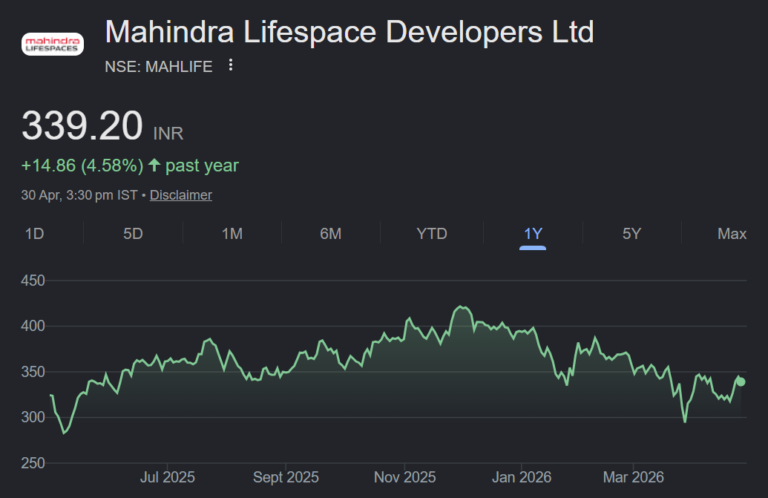

The company retained its pre-sales guidance of ₹ 4500-5000 crore for FY27 while it...

BAF continues to reinforce its positioning as a high-quality compounding franchise, underpinned by strong...

Growth in the India consumer business continues to be driven by power brands and...

In Q4FY26, FD NOV growth accelerated to 18.8% YoY (down 0.9% QoQ) to INR...

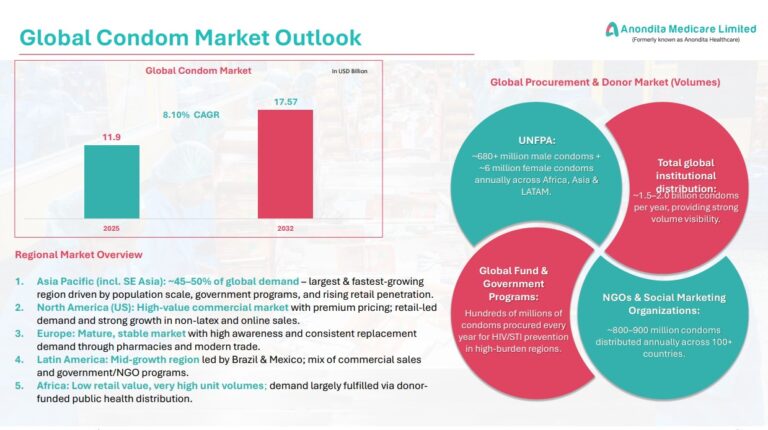

The company operates in a structurally growing market. The global condom market is expected...