The company has revised its guidance for revenue growth to be around Rs 3,000...

As of Dec’25, MAN’s aggregate executable order book stands at ~Rs 4,000 cr, providing...

It continues to gain market share across categories, with particularly strong momentum in BLDC...

Jubilant Pharmova (JPL) is an integrated, multi-dimensional pharmaceuticals company with global presence.

Existing hospitals sustained strong performance, delivering a robust 33% YoY revenue growth

The company has maintained a healthy order book of ₹ 1685 crore (as on...

PGIL’s diversified business model brings in more resilience in the performance with revenues and...

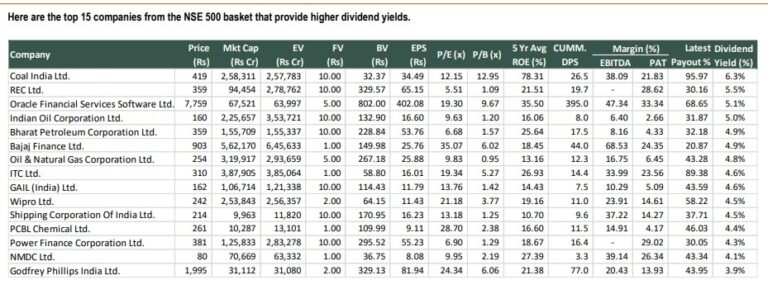

top 15 companies from the NSE 500 basket that provide higher dividend yields

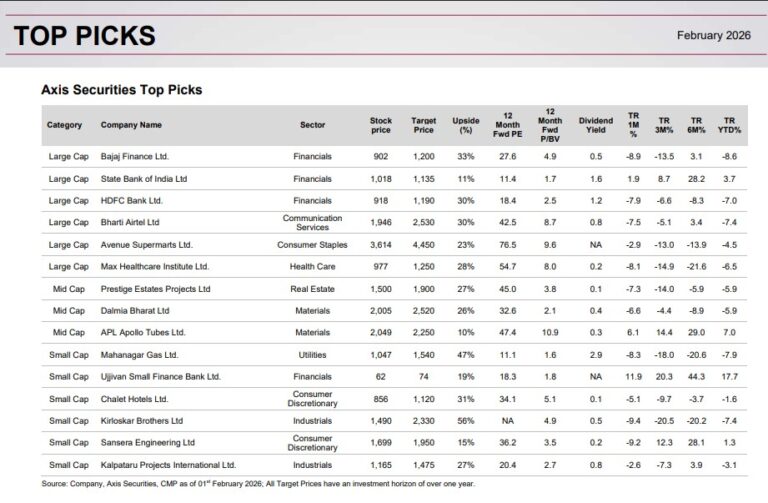

We have updated our Top Picks by replacing Inox Wind with Dalmia Bharat Ltd,...

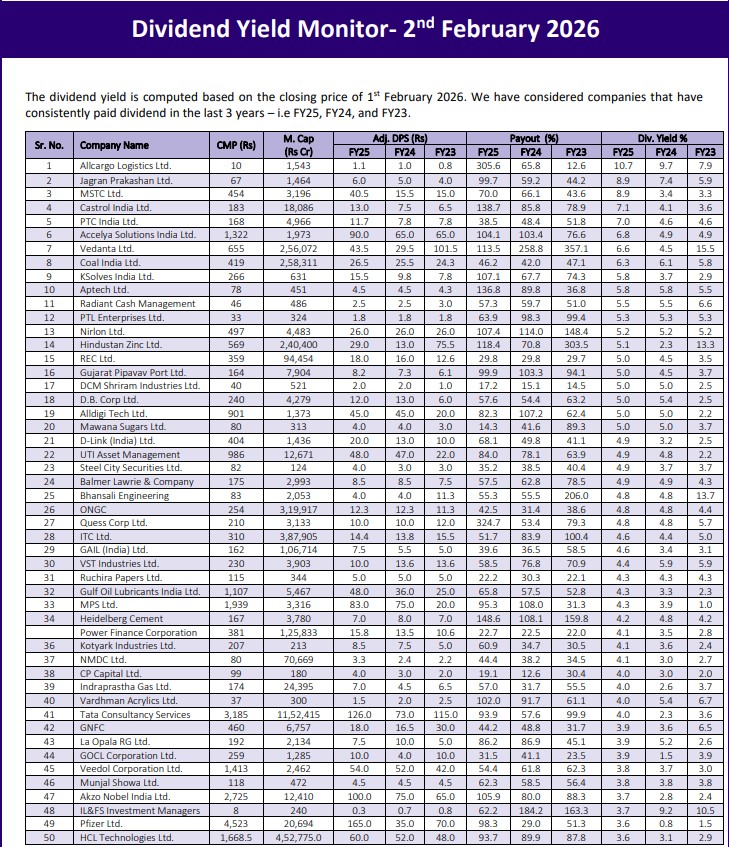

dividend yield is computed based on the closing price of 1st February 2026