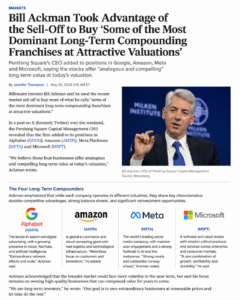

Ackman’s strategy reflects a classic long-term investing philosophy: buy extraordinary businesses during periods of...

Arjun

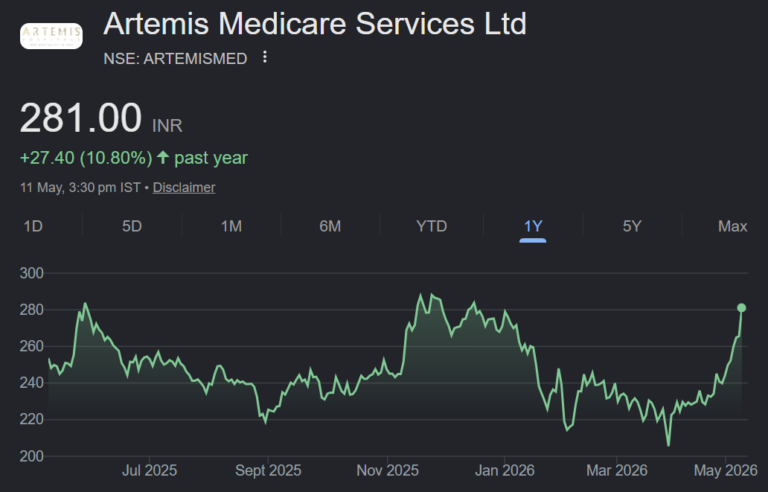

DLF conservatively guided for launch and pre-sales of ₹ 20,000 crore for FY27 (FY26...

We continue to like TVSL on a structural basis, due to its premiumization-led growth,...

Oberoi realty is expected to recoup the lost opportunity in FY27 in terms of...

IHCL’s capital light strategy is a key competitive advantage over other branded hotel companies...

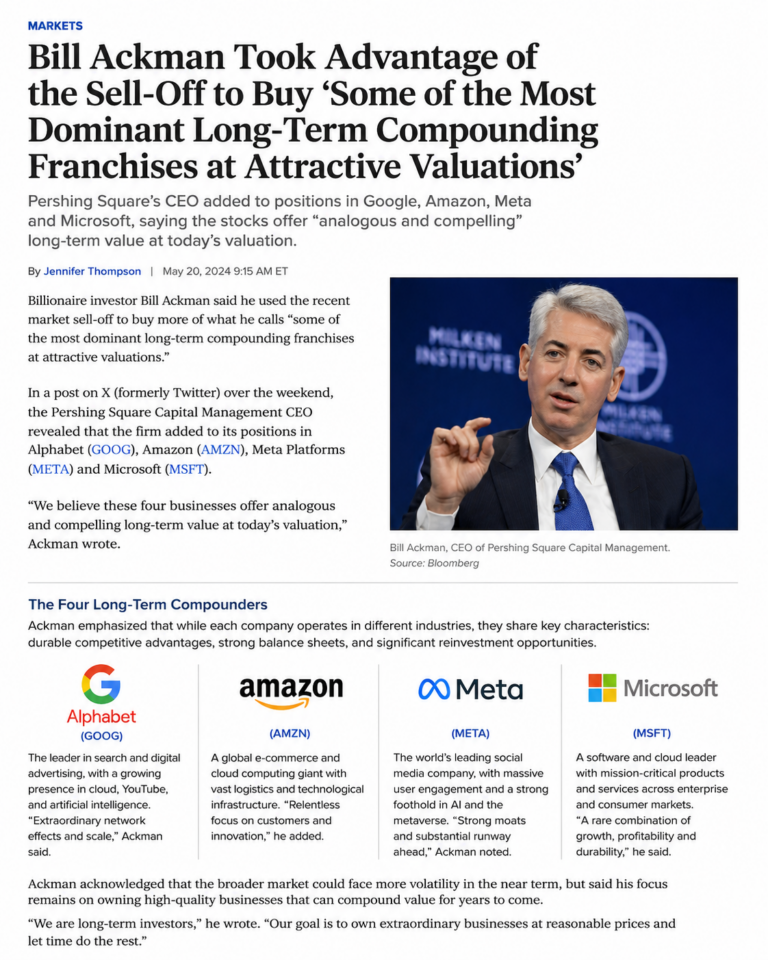

Artemis Medicare Services Ltd (Artemis) is a healthcare venture launched by the promoters of...

We feel most negatives are now behind except concerns around ADD. Lowering conversion cost,...

Premiumisation and D2C play will help AFL revenues/EBIDTA/PAT to grow by 14%/18%/38% respectively.

Market veteran Ashish Kacholia, known for spotting "multibagger" midcaps, has been a major catalyst...

Dolly Khanna is known for her "bottom-fishing" strategy—buying into companies when they are out...