BAJEL is on the cusp of a healthy growth trajectory

Arjun

Luxury travelers are increasingly planning trips around experiences such as celebrations, wellness, culinary immersion,...

With levers of growth, Sandhar trades inexpensive at <20x P/E and <10x EV/EBITDA on...

The company aims to capitalize on the strong structural tailwinds within the hospitality space...

The ultra-pure water segment is an emerging segment and is expected to be an...

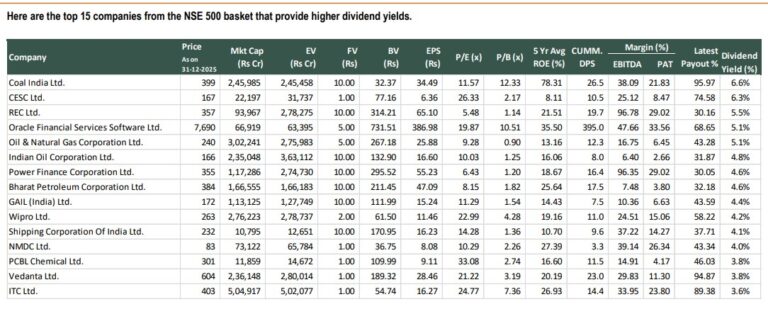

top 15 companies from the NSE 500 basket that provide higher dividend yields

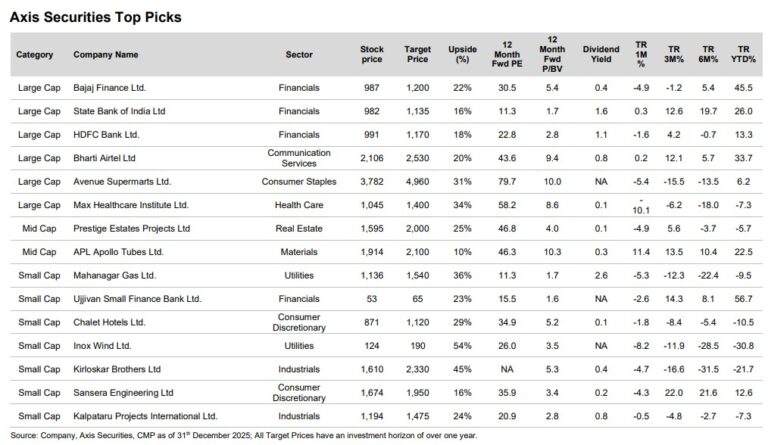

We maintain our Top Picks recommendations unchanged for the month as we continue to...

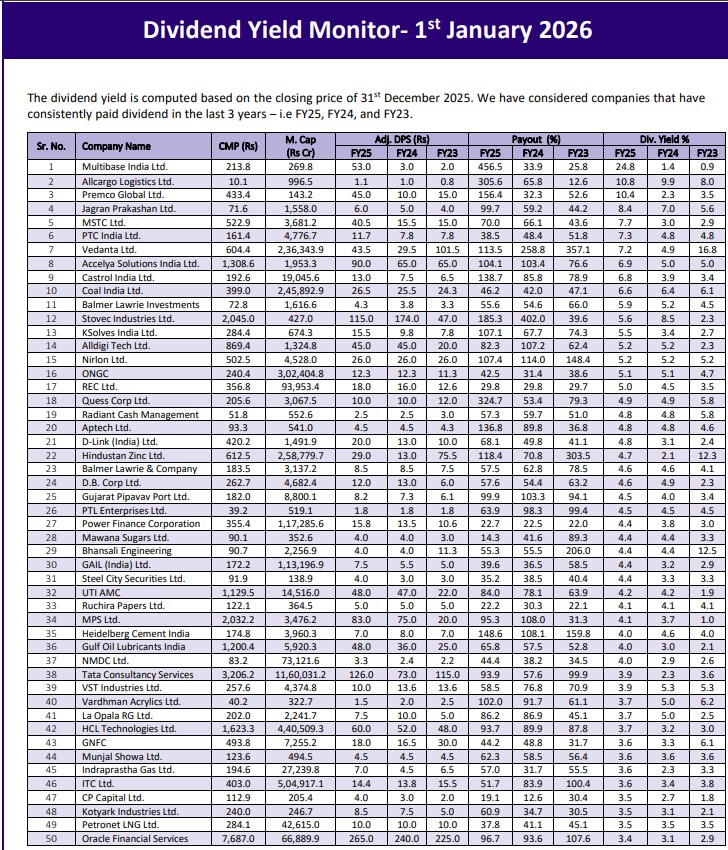

Multibase India Ltd has paid Rs 53 per share as interim dividend in Nov’24

We expect V-Mart to deliver a robust ~18% revenue CAGR over FY25-28, driven by...

Management reiterated its focus on optimising topline mix to yield superior GMV-revenue conversion and...