Accelerating Growth with Stable Margins; Upgrade to Buy

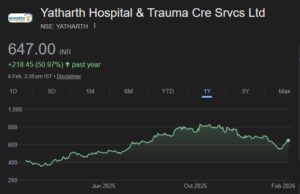

Yatharth Hospital delivered a stellar Q3FY26 performance, well ahead of our estimates, with revenue rising 46% YoY to Rs 3,205 mn, led by robust growth in the Noida cluster and ramp-up at newer units. EBITDA grew 35% YoY to Rs 742 mn, and adjusted EBITDA margin, excluding initial losses at the three new hospitals, improved to ~29%, reflecting strong operating leverage. Occupancy remained among the highest in the sector, with Noida at 91%, Greater Noida at 74% and Jhansi at 72%, alongside healthy volumes at Faridabad, Greater Faridabad and Model Town Delhi. ARPOB rose ~10% YoY to ~Rs 33,744, driven by a richer mix of complex super-specialties and oncology. Adjusted PAT was up ~80% YoY, while reported PAT rose ~50% YoY, underscoring strong earnings scalability despite dilution from new facilities. The recently acquired 250‑bed Agra Super Specialty NABH hospital, already EBITDA positive, is expected to contribute meaningfully from Q4 as robotics and additional super specialists ramp up. Management plans to roughly double capacity over the next 3–4 years, while targeting receivable days below 110 by FY26-end. With sustained 10% ARPOB growth, a rising oncology mix, lower ramp‑up losses and a strong net cash position, we see scope to raise FY26E–28E revenue estimates while assuming consolidated EBITDA margins in the 24–25% band, with core operations already delivering 28–29% margins. We value the stock at 16x FY28E EV/EBITDA (from 18x earlier) to reflect a calibrated stance on a sustained margin ceiling under a continuous expansion regime, arriving at a revised target price of Rs 855 per share and upgrade the stock to Buy.

A Strong performance for the quarter

• In Q3FY26, the company reported Rs. 3,205 Mn revenue, a 46% YoY Increase. New Hospitals led the growth momentum, with New Delhi and Faridabad Sec-20 contributing Rs.279 Mn in revenue – 9% to Group’s revenues – within first full quarter of operations.

• EBITDA grew by 35% YoY and by 15% sequential basis to Rs. 742 Mn, with margins contracted by 189 bps YoY and remain flat on sequential basis to 23.2%

• Overall occupancy for the hospitals improved to 67% compared to 60% in Q3FY25 and Inpatient volumes up 29% YoY and outpatient volumes up 11% YoY with ALOS stand at 4.3 days. ARPOB for hospitals was up by 10% YoY to Rs. 33,744.

• Existing hospitals sustained strong performance, delivering a robust 33% YoY revenue growth. Noida Extension recording its highest-ever ARPOB at Rs. 44k (+16% YoY).

Outlook and Valuation: Yatharth is well placed to deliver strong, compounding growth, supported by high Q3 momentum and a richer super-specialty/oncology mix. Continuous capacity expansion will keep reported margins capped below 25% but should significantly lift absolute EBITDA and PAT. A strong net cash balance sheet, improving receivable days and the EBITDA‑accretive Agra acquisition further de‑risk execution and support planned brownfield projects. Balancing superior growth visibility with an expansion‑led margin ceiling, we value Yatharth at 16x (from 18x) FY28E EV/EBITDA, arriving at TP of Rs 855 implying ~33% upside and upgrade the stock to Buy.

Yatharth Hospital and Trauma Care Services Ltd – Q3FY26 Result Update – SMIFS Institutional Research