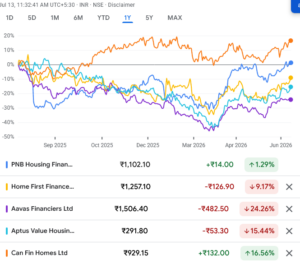

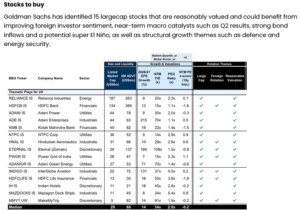

Growth steady, earnings absorb provisioning…

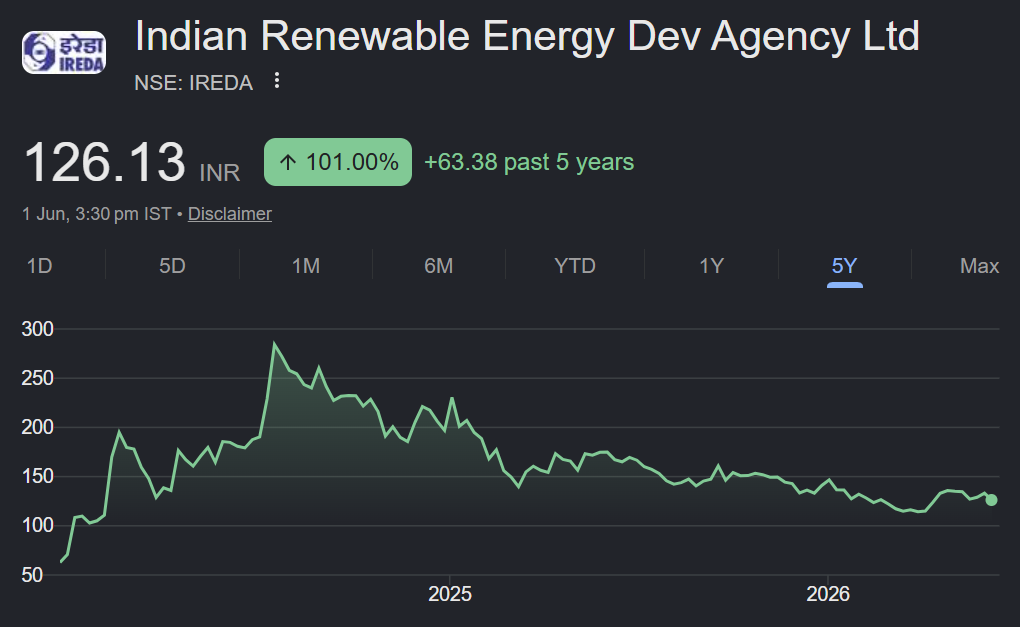

About the stock: IREDA is a systemically important non-deposit taking non- banking financial company engaged in financing of renewable sector.

• The company has geographically diversified asset base with term loans outstanding across 23 states and 4 union territories across renewable segment.

Q4FY26 performance: IREDA delivered mixed Q4FY26 performance, sustaining AUM growth at ~22% YoY (6% QoQ) to ₹93,069 crore, driven by continued disbursement momentum across renewable energy segment. NII grew 18.5% YoY (3.2% QoQ) to ₹897 crore, supported by balance sheet expansion and lower cost of borrowings at 7.05% (vs 7.61% in FY25). NIM improved to 3.65% (-9bps/38 bps QoQ/YoY). PAT declined 1.8% YoY to ₹493 crore owing to elevated provisioning of ₹215 crore and forex loss. Asset quality continued to show normalization trend, with GNPA/NNPA declining ~26/39 bps QoQ to 3.49%/1.29% respectively and PCR improving ~780 bps QoQ to 63.9%.

Investment Rationale

• Sustained growth momentum with steady return profile: IREDA continues to deliver healthy balance sheet expansion, supported by strong disbursement and increasing financing demand across India’s renewable ecosystem. Diversification beyond solar & utilities into manufacturing, storage and emerging technologies should support healthy advances growth of ~24-25% CAGR over FY26–28E. Despite moderation in spread/NIM, operating leverage is expected to sustain ~2% RoA.

• Strengthening provisioning buffer to support earnings stability: Q4FY26 reflected a more conservative provisioning approach, strengthening confidence on sustainability of portfolio quality despite near-term profitability pressure. Management’s prudent risk recognition, improving portfolio seasoning and disciplined underwriting are expected to support lower incremental stress ahead. We expect improving portfolio seasoning and conservative provisioning to keep credit cost contained to ~60-70 bps over FY26–28E, aiding earnings trajectory.

• Long term growth opportunity supported by funding profile: Government’s focus on scaling renewable energy capacity from ~275 GW currently to 500 GW by FY30 continues to provide a multi-year growth runway for IREDA. Its strategic role in renewable financing, diversified sector exposure and expanding footprint across emerging areas including manufacturing, storage and energy-transition infrastructure position it well to capture incremental financing demand. Additionally, strengthening capital base and access across domestic borrowings and ECBs enhance funding flexibility and support future growth while preserving long-term profitability profile.

Rating and Target Price

Despite moderation in profitability due to higher provisioning, Q4FY26 performance reflects continued normalization in asset quality and healthy balance sheet growth. While growth runway remains a tailwind with sustained return ratios, there exists inherent risk of volatility given lumpy exposure. We value the stock at ~2.6x FY28E BV and maintain BUY rating and maintain target price of ₹ 180.