Global investment firm Goldman Sachs has invested ₹65 crore in Cera Sanitaryware, highlighting continued institutional interest in one of India’s leading sanitaryware companies. With a market capitalization of around ₹7,200 crore, Cera has built a strong presence across sanitaryware, faucets, bathroom fittings and allied products.

Cera is a dominant player in the Indian sanitaryware market, offering products across multiple price segments — from mass-market offerings to premium solutions. The company has benefited from the long-term trends of urbanization, rising disposable incomes, housing demand and increasing consumer preference for branded bathroom products.

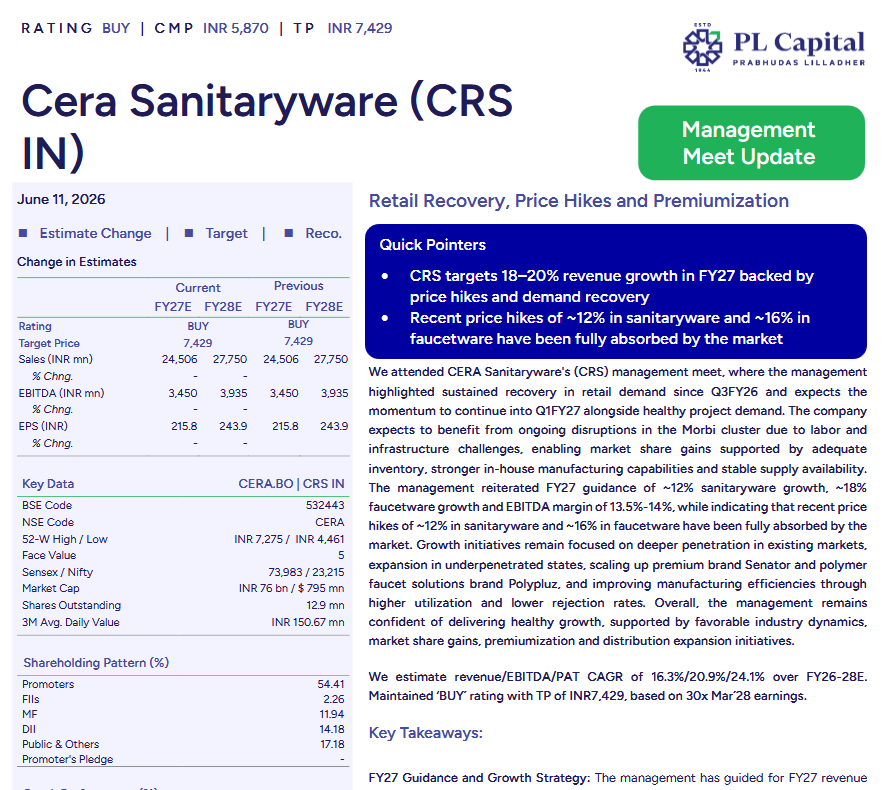

Strong Ownership & Financial Profile

Cera Sanitaryware has a strong promoter backing, with promoters holding 54.41% stake. Institutional confidence is reflected through investors such as Nalanda Equity Fund, which holds around 9.57% stake.

The company maintains a robust balance sheet with zero debt and cash reserves of approximately ₹757 crore. It has consistently generated healthy returns, with Return on Equity (RoE) at around 18.33%. Cera has also maintained a consistent dividend payout track record, making it attractive for long-term investors seeking both growth and financial stability.

Growth Drivers: Retail Recovery, Price Hikes & Premiumization

According to a recent management interaction, Cera has witnessed sustained recovery in retail demand since Q3FY26, with momentum expected to continue into Q1FY27. The company is also seeing healthy demand from the project segment.

The management expects FY27 growth to be driven by:

- Recovery in retail demand

- Price increases across product categories

- Premiumization of product mix

- Expansion into underpenetrated markets

- Stronger distribution network

Cera recently implemented price hikes of around 12% in sanitaryware and approximately 16% in faucetware. These price increases have been fully absorbed by the market, indicating healthy demand conditions and pricing power.

Opportunity From Industry Disruptions

The company believes ongoing challenges in the Morbi cluster, including labour shortages and infrastructure issues, could provide an opportunity for organized players like Cera to gain market share.

With adequate inventory levels, stronger in-house manufacturing capabilities and stable supply availability, Cera is positioned to benefit from customers shifting towards reliable branded manufacturers.

Focus on Premium Brands & Manufacturing Efficiency

Cera continues to strengthen its premium portfolio through brands such as Senator, while also scaling newer categories like polymer faucet solutions under Polypluz.

The company is also focused on improving manufacturing efficiency through:

- Higher capacity utilization

- Lower rejection rates

- Better operational productivity

These initiatives are expected to support margin expansion over the medium term.

Brokerage View: Buy Rating With ₹7,429 Target

Prabhudas Lilladher has maintained a Buy recommendation on Cera Sanitaryware with a target price of ₹7,429, implying an upside of around 27% from the current market price of ₹5,850.

The brokerage expects Cera to deliver strong earnings growth, estimating revenue, EBITDA and PAT CAGR of approximately 16.3%, 20.9% and 24.1% respectively over FY26-FY28E.

The target valuation is based on around 30x March 2028 earnings.

Outlook

Cera Sanitaryware appears well positioned to benefit from India’s shift towards organized branded home improvement products. A debt-free balance sheet, strong brand equity, premiumization strategy and improving demand environment provide multiple growth levers.

With institutional investors increasing exposure and analysts expecting healthy earnings growth, Cera remains a key company to watch in India’s building materials and consumer durables space.

Earlier, the brokerage/institutional recommendation report used to be attached with the recommendation coverage by Rakesh Jhunjhunwala site. But this practice has been stopped from some time.

It is requested to please attach the recommendation/research coverage report also along with your coverage of the same.

Thank you.