Strong order pipeline and margin support growth visibility…

About the stock: Kilburn Engineering Limited (KEL), incorporated in 1987, largest player in customised drying solutions and process equipment. With a strong proprietary technology base in drying systems, the company has established itself as a niche solutions provider.

• Their products find applications across multiple sectors such as chemicals, petrochemicals, fertilizers, carbon black, pharma, food, oil & gas, power (including nuclear), metals and cement etc.

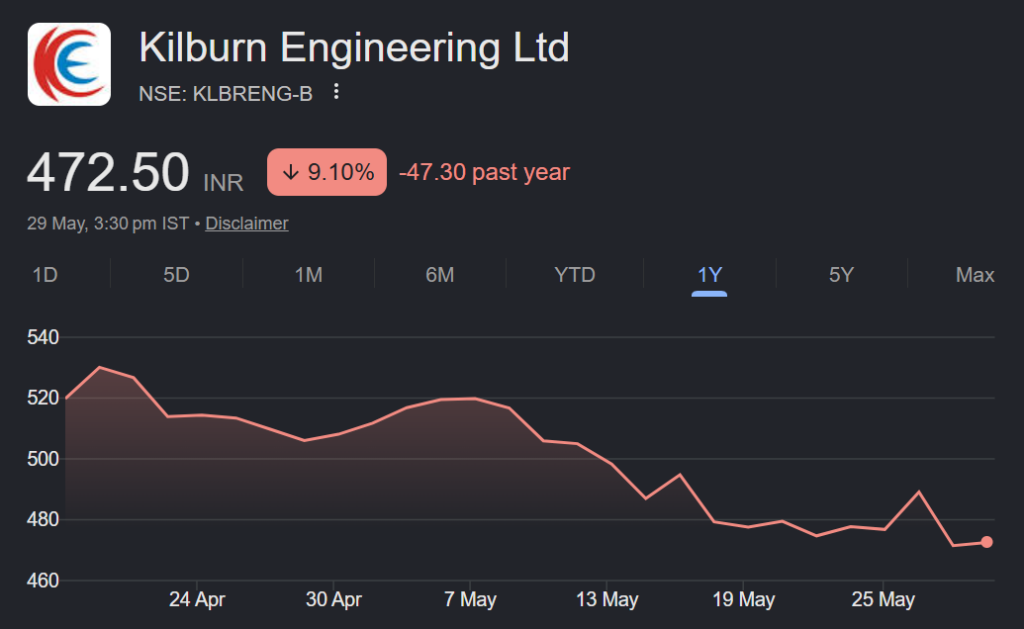

• The company has strategically transitioned from a product supplier to a comprehensive solution provider resulting in Revenue and PAT CAGR of 41.6% and 25% over FY23-26, respectively. Q4FY26 performance: Kilburn Engineering reported Q4FY26 performance with revenue rising 49.0% YoY to ₹189.2 crore, while EBITDA increased 5.3% YoY to ₹37.7 crore. EBITDA margin moderated sharply to 19.9% versus 28.2% in Q4FY25 due to normalization in product mix and higher material costs. PAT grew 21.8% YoY to ₹24.9 crore. For FY26, revenue grew 48.1% YoY to ₹628.8 crore, EBITDA increased 44.5% YoY to ₹147.1 crore with EBITDA margin at 23.4% vs 24% YoY, while PAT rose 53.8% YoY to ₹96.2 crore. The company also turned net debt free after completing a ₹300 crore fund raise and reported an unexecuted order book of ₹467 crore.

Investment Rationale:

• Sustainable EBITDA margin and scalable business model support profitable growth: Kilburn continues to maintain among the highest profitability levels within the engineering EPC sector, with consolidated FY26 EBITDA margin of 23.4% despite macroeconomic disruptions and supply chain challenges. Management reiterated sustainable margin guidance of 22–23%, supported by strong execution capabilities, diversified product portfolio and disciplined cost management. The company has already demonstrated meaningful operating leverage, scaling from a ~₹100–200 crore revenue business to nearly ~₹630 crore consolidated revenue while maintaining strong profitability. Further, ongoing capacity expansions at Saravali and ME Energy are expected to support future growth till FY28 without requiring significant additional capex, strengthening return ratios and cash-flow generation.

• Diversified industrial exposure and strong inquiry pipeline support sustained growth visibility: Company continues to benefit from strong demand across diversified industrial sectors including fertilizers, petrochemicals, sludge processing, nuclear, steel, offshore gas recovery and specialty chemicals. The company currently has a robust inquiry pipeline exceeding ₹4,000 crore and is targeting order inflows of ₹800– 1,000 crore in FY27, providing strong medium-term growth visibility. Management also highlighted that several large orders delayed due to geopolitical disruptions are expected to be finalized over the next 2–3 months. Additionally, growing opportunities in waste heat recovery systems, sludge processing and nuclear applications further strengthen long-term demand visibility across Kilburn and its subsidiaries.

Rating and Target Price

• We expect Revenue and PAT to grow at 19.4% and 17.9% CAGR over FY26-FY28E. We maintain Buy on KEL with a Target Price of ₹650 (based on 23x P/E on FY28E EPS)