➢ Lloyds Metals And Energy (LMEL) has acquired a 49% stake in Virtus Lloyds Minerals Holding (VLMH) for US$ 30mn; VLMH holds 100% of CHEMAF, which owns 50+ copper and cobalt mining permits in the DRC.

➢ Media reports indicate the transaction involved funding commitments and restructuring of CHEMAF’s debt, suggesting a stressed asset turnaround opportunity.

➢ This marks LMEL’s second DRC acquisition; at peak, combined assets could scale to 100ktpa copper and 20ktpa cobalt, alongside ~50mtpa mining volumes by Thriveni.

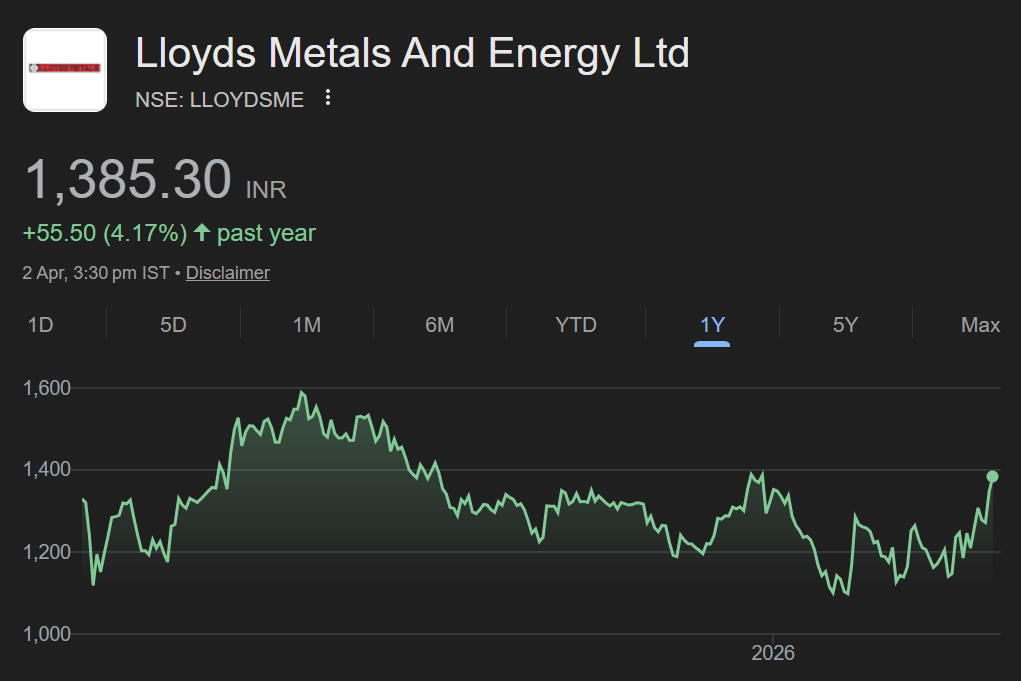

➢ Maintain LONG with an unchanged SOTP-based Mar’27 TP of Rs 2,100.

Debt-led entry into CHEMAF; strategic resource access: As per media articles (Link here), Virtus Minerals’ acquisition of CHEMAF was structured around significant capital infusion, including funding for stalled projects and the assumption/restructuring of existing debt. This indicates a capital-constrained asset, with value creation contingent on execution and balance sheet repair. The transaction is part of a broader US-led push to secure critical mineral supply chains and reduce reliance on China, supported by the US–DRC strategic partnership framework.

LMEL builds DRC platform via VLMH: LMEL has acquired a 49% stake in VLMH (30th Mar’26, link here) via its wholly owned subsidiary LGRF for US$ 30mn. VLMH is a JV with Virtus Minerals (51%), providing LMEL indirect exposure to CHEMAF. The asset base includes the Etoile facility (20ktpa copper, 4ktpa cobalt) and the Mutoshi expansion (50ktpa copper, 16ktpa cobalt), located in the Katanga Copper Belt. The transaction positions LMEL within a US-aligned critical minerals ecosystem, with the DRC accounting for >70% of global cobalt reserves and being a key copper-producing region.

Platform buildout with execution lever: LMEL’s DRC strategy is evolving into a scalable copper–cobalt platform, with two assets now in place (Exhibit 1). At peak, combined capacity could reach ~100ktpa copper and ~20ktpa cobalt, alongside ~50mtpa mining volumes by Thriveni, driving product and geographic diversification. While the CHEMAF asset appears to involve balance sheet repair, we see this as an opportunity for value creation, contingent on execution. Strong cash flows from the domestic iron ore business provide funding visibility for this expansion.

Key monitorable and risks: Execution of the CHEMAF turnaround will be key, particularly timelines for completion and ramp-up of the Mutoshi project, along with visibility on debt restructuring and funding requirements. Strategically, the acquisition enhances LMEL’s exposure to energy transition metals, where copper and cobalt demand remains structurally strong. Key risks include execution slippages, higher capital intensity, balance sheet repair at CHEMAF, and geopolitical/regulatory risks in the DRC, along with commodity price volatility.