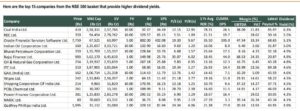

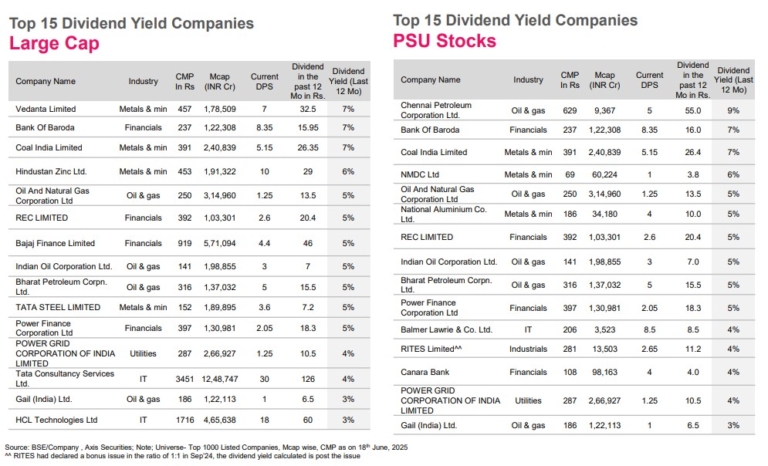

Top 15 Dividend Yield Companies as of 18th June 2025 in Large Cap, PSU...

We initiate coverage on Swiggy with a BUY rating and 12-mth DCF based target...

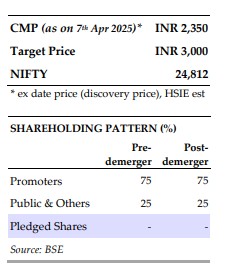

Siemens Energy India Ltd (SEL) captures the maximum value among its peers as it...

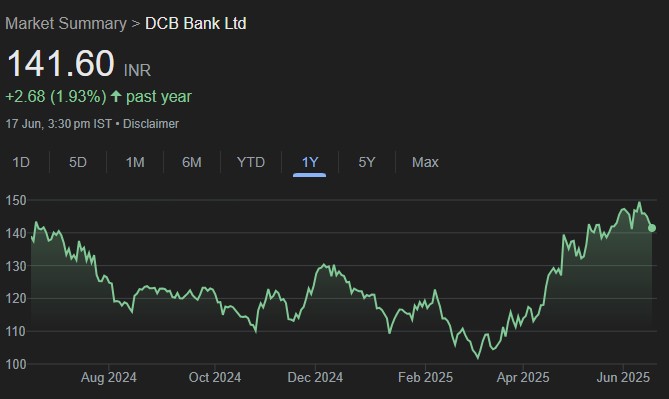

We met Mr Praveen Kutty, MD&CEO of DCB Bank (DCB). Highlights: 1) Management is...

Over the past 10 years, GALSURF has demonstrated its ability to scale profitably while...

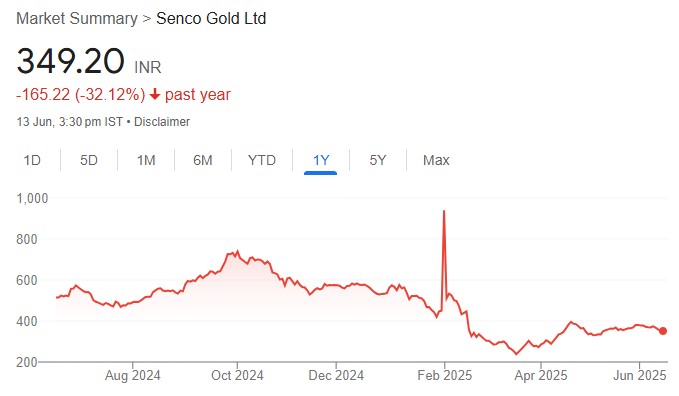

Senco Gold posted strong growth across Revenue/EBITDA/PAT of 21.1%/44.8%/94.1% YoY respectively led by healthy...

Ather Energy will remain one of the leading players through the EV transition. It...

We interacted with Repco Home Finance’s Management to understand the drivers of loan growth...

We attended the analyst meet hosted by Juniper Hotels wherein the company highlighted its...

We initiate coverage on Time Technoplast (TIME) with a BUY rating and a target...