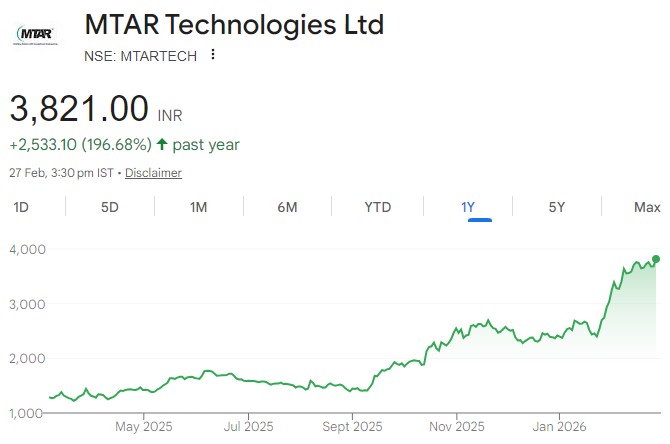

MTARTECH is firmly positioning itself as the indirect beneficiary of the global AI infrastructure...

Outlook for the wind industry is positive over the medium to long term, given...

ZF combines high margin technology products with a stable and growing aftermarket business, providing...

Asset quality remains a key strength for Capri Global, supported by its predominantly secured...

A key inflection in NACL’s evolution has been its calibrated yet decisive transition from...

Volume growth expected at ~13% CAGR over FY25-28E; Doubling capacity by FY29E

The company has taken significant steps to enhance operational efficiencies including improvements in sourcing,...

In the Union Budget 2026-27, announcements were made for 7 new bullet train corridors,...

SHL has the capability to manufacture oral liquids, tablets, injectables, dry powder & inhaler...

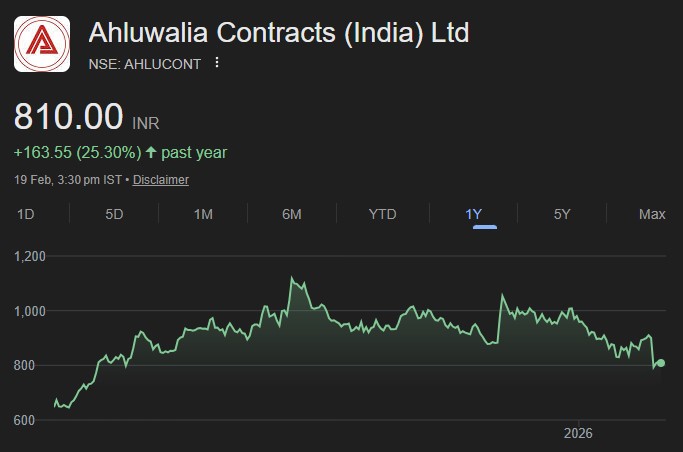

With robust inflows of c.INR 59bn (ex GST) in 9MFY26, ACIL’s backlog strengthened to...