The benchmark indices moved in a very narrow range throughout the last month after rallying hard in September this year. The Nifty and the Sensex ended the month with marginal losses of 0.2% and 0.7% respectively (the data is from September 28 to October 26, 2012). Within the Top Picks basket, some of the recent entrants like Axis Bank, Persistent Systems and Godrej Consumer Products reported healthy gains of 7-10% each for the period. However, the out-performance of the Top Picks basket was limited by the unexpected controversy in IRB Infrastructure Developers (IRB) that resulted in a sharp sell-off in the stock (the stock fell by 21.5% in this period). Consequently, the Top Picks basket performed in line with the benchmark indices and reported a marginal decline of 0.5% for the period under review.

For the current month, we are making two changes in the Top Picks basket. We are introducing Mahindra and Mahindra (M&M) in place of IRB in accordance with the recent change in our automobile (auto) analyst’s view on the sector (from bearish to positive). Our auto analyst believes that the volume growth would pick up in some segments of the sector, like tractors and passenger cars, from the next quarter. The removal of IRB is more of a cautionary step due to the weakening of sentiments towards the stock in the wake of two controversies related to the IRB’s management in a short time. The other change is the replacing of Mcleod Russel with Relaxo Footwear. We are bringing in Relaxo Footwear because we believe it is a good proxy play on the domestic consumption story as well as a likely beneficiary of the prevailing soft rubber prices.

Axis Bank is attractively valued as it trades at 1.6x FY2014 book value against a five-year mean valuation of 2.2x. We expect the bank to deliver return on equity (RoE) of ~19% and return on asset (RoA) of 1.5% by FY2014. We recommend a Buy on Axis Bank with a price target of Rs1,370.

Bharat Heavy Electricals Ltd (BHEL) is a premier power generation equipment manufacturer and a leading engineering, procurement and construction company. The relatively lower order intake in recent years would reflect on its revenue growth and result in a marginal decline in the earnings over the next two years. However, a lot of negatives are reflected in the serious de-rating of the stock over the last two years. Therefore, we have included BHEL in our Top Picks basket.

Cadila Healthcare: We expect revenue compounded annual growth rate (CAGR) of 18.6% and profit CAGR of 25.6% over FY2012-14. The stock is currently trading at 13.9x FY2014E earning per share (EPS), which is a 19% discount to Lupin. We believe the valuation discount should narrow further. We value the stock at 17x FY2014E EPS to arrive at a price target of Rs1,064.

Dishman Pharma: The stock is currently trading at 5.4x FY2014E EPS, which is a 60% discount to its five-year average P/E multiple and close to a 68% discount to Divi’s Laboratories. We expect the valuation gap to narrow on a strong operating performance and an improved financial health. We recommend a Buy on the stock with a price target of Rs135 (8x FY2014E EPS).

Godrej Consumer Products Ltd (GCPL): We believe the increased competitive activity in the personal care and hair care segments and the impact of high food inflation on the demand for its products are the key risks to the company’s profitability. At the current market price, the stock trades at 30.0x its FY2013E EPS of Rs23.6 and 24.4x its FY2014E EPS of Rs 29.0.

ICICI Bank: The stock trades at 1.7x FY2014E book value. We expect the stock to re-rate, given the improvement in the profitability led by lower NPA provisions, a healthy growth in the core income and improved operating metrics. We recommend Buy with a price target of Rs1,230.

Larsen & Toubro (L&T), the largest engineering and construction company in India, is a direct beneficiary of the strong domestic infrastructure development and industrial capital expenditure (capex) boom. Sound execution track record, bulging order book and strong performance of its subsidiaries reinforce our faith in L&T. With the company entering new verticals, namely solar and nuclear power, railways, and defence, there appears a huge scope for growth. At the current market price, the stock is trading at 19.4x its FY2014E stand-alone earnings and at an EV/EBIDTA of 11x.

Mahindra & Mahindra (M&M): The company’s pricing power is better compared with the other OEMs because of its strong brand equity. It took price hikes aggressively to maintain the margins in both the automotive and the farm equipment division. The company is expected to launch Reva electric NXR and sub-four meter Verito in H2FY2013. Our SOTP-based price target for M&M is Rs949 per share as we value the core business at Rs721 a share and the subsidiaries at Rs228 a share. We recommend Buy on the stock.

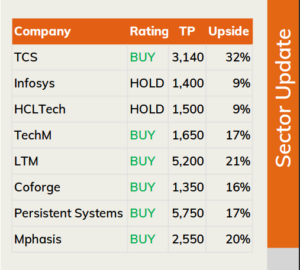

Persistent Systems Ltd (PSL) is a niche player in the highly under-penetrated outsourced product development (OPD) market. PSL has helped its customers develop over 3,000 products over the last five years. With strong domain expertise and years of experience in the OPD business, PSL is well placed to garner the incremental spending taking place in the global R&D space. Its earnings are expected to grow at a CAGR of 23.5% over FY2012-14. At the current market price, the stock trades at 10.5x and 8.7x FY2013 and FY2014 earnings estimates respectively.

Relaxo Footwear is present in the Indian organised footwear market and is involved in the manufacturing and trading of footwear through its retail and wholesale networks. The company’s top brands, namely Hawaii, Sparx, Flite and Schoolmate, have an established presence among their respective segments. At the current market price, the stock trades at 17.4x its FY2013E EPS of Rs41.7 and 12.3x its FY2014E EPS of Rs59.2.

Reliance Industries Ltd (RIL) has a strong presence in the refining, petrochemical and upstream exploration business. The refining division of the company is the highest contributor to the company’s earnings and is operating efficiently with a better gross refining margin (GRM) compared with its peers in the domestic market due to the ability of its plant to refine more of heavier crude. However, the gas production from the Krishna-Godavari-D6 field has fallen significantly in the past one year. With the government approval for additional capex, we believe production will improve going ahead. The key concern remains in terms of a lower than expected GRM, profitability of the petrochemical division and the company’s inability to address the issue of falling gas output in the near term. At the current market price the stock is trading at PE of 12.3x its FY2014E EPS,” says Sharekhan research report.

ShareKhan’s Model Portfolio Of Top Stocks

[download id=”329″]