The integration of Ecom Express is set to enhance network efficiency and reduce capital...

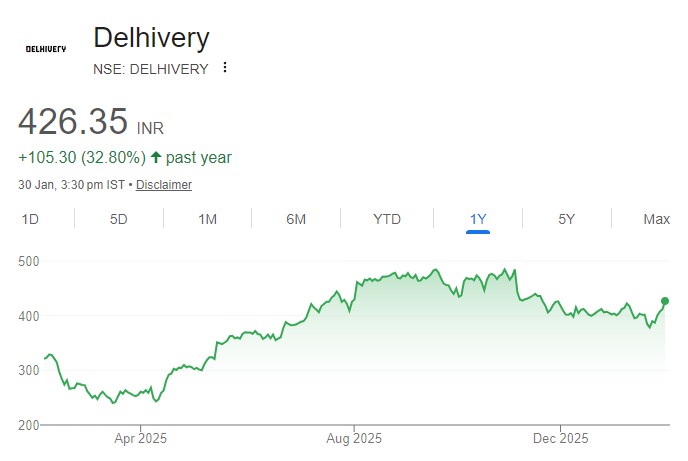

Delhivery share price target

Delhivery is well-positioned for future growth, supported by strong momentum in its core transportation...

Delhivery has outperformed the market since announcing the acquisition of Ecom Express, we believe...