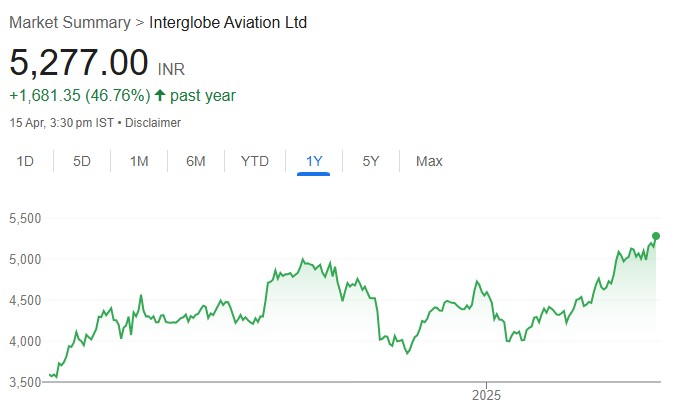

We upgrade INDIGO to BUY as we believe that benign Brent crude prices amid...

Indigo

Gautam Shah, a noted expert on technical analysis, has sent the chilling warning that...

Saurabh Mukherjea has recommended that we buy stocks which have a competitive advantage moat...

The PMS Funds of Porinju Veliyath & Basant Maheshwari are hapless victims in the...

Mudar Patherya has homed in on five micro-cap stocks which he describes as “rainbow...

Eminent investors such as Raamdeo Agarwal, Shankar Sharma, Saurabh Mukherjea, Kenneth Andrade and Akash...

Radhakishan Damani, who once suffered the ignominy of being booted out of the Forbes...

Mohnish Pabrai & Guy Spier, both eminent value investors, have declared that they are...

Shankar Sharma has sensibly recommended a media stock which is known for its strong...

Raamdeo Agrawal, the boss man of Motilal Oswal, recommended a stock on the basis...