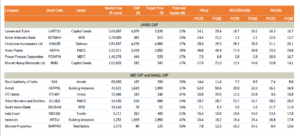

Cairn India CMP – Rs.328, Current TP – Rs.365

Cairn India Ltd (CIL) is one of the biggest private exploration and production companies in India.

MBA have recoverable oil reserves and resources of more than 1 billion barrels, which includes proven plus probable (2P) gross reserves and resources of 636 million barrels of oil equivalent (Mn boe) with a further 308 Mn boe or more of enhanced oil recovery (EOR) potential. This is 25-30 years of production.

Based on our estimates, the stock is trading at 5.1x EV/EBIDTA and 6.3x P/E on FY14E earnings.

ICICI Bank CMP – Rs.1077, Current TP – Rs.1286

ICICI bank is better placed vis-à-vis its peers with robust liability franchise (CASA mix at ~41% at the end of Q2FY13), stable asset quality, improving NIM (3%+ during last 3 Quarters).

Management’s focus on stable growth with improving structural profitability (RoE is likely to improve further with increase in leverage in next 2-3 years) reinforces our existing positive outlook on the stock.

Retail book, which constitutes ~35% of total loan book, has seen near nil slippage during last couple of quarters; this has made us more confident on its overall asset quality.

After stripping off the value of subsidiaries (Rs.204), stock is trading reasonable at 1.4x its FY14 ABV.

Grasim Industries CMP – Rs.3356, Current TP – Rs.3662

Grasim Industries is a diversified player in cement, viscose staple fibre (VSF) and chemicals and is also expanding its capacity in cement to enhance its overall market share in cement and VSF division to capture higher demand.

We thus expect company to benefit from volume expansion as well as pricing improvement going forward.

Along with this, company also has a healthy balance sheet and is open for further expansion in cement capacity through organic or inorganic means.

It is trading at very attractive valuations of 9.4x P/E on FY14 estimates.

Tata Consultancy Services CMP – Rs.1329, Current TP – Rs.1460

The management has maintained its optimism of beating NASSCOM’s target growth rate of 11% – 14% (USD terms) in FY13 in CC terms and has also maintained an optimistic macro outlook.

TCS’ revenue growth in the past few quarters has been better than Infosys and it has been able to restrict impact on margins.

Stock is available at about 18x FY14 estimates

Adani Port (ADSEZ) CMP – Rs.130, Current TP – Rs.156

ADSEZ has outlined aggressive plans to emerge as one of the largest private port operators in India.

Total cargo handling capacity for the company in India is expected to increase from 150mn tons currently to 225mn tons by FY14E.

As a large portion of the volumes is linked to energy imports, we expect volumes for the port to grow at 18% CAGR to 90mn tons by FY14E.

Stock is trading at very attractive valuations of about 13.3x on FY14 estimates.

Engineer’s India Ltd CMP – Rs.227, Current TP – Rs.275

Engineers India Ltd (EIL) is India’s leading publicly held company engaged in the areas of hydrocarbon, metals and infrastructure consultancy.

According to Ministry of petroleum and natural gas, domestic crude oil refining sector is likely to significant capacity in twelfth five year plan. EIL is likely to benefit from this as it enjoys entrenched relationship with PSU majors like HPCL, BPCL, IOC etc.

In order to widen its spectrum of offerings, company has entered into various favourable joint ventures with domestic as well as international players.

Stock is trading at very attractive valuations of about 10.1x on FY14 estimates.

KPIT Cummins CMP – Rs.121, Current TP – Rs.146

Management commentary echoes the optimism sounded by other leading peers about the continuing traction in automotive, manufacturing and hi-tech verticals, the mainstay of KPIT.

We understand that, the company has decent visibility on revenues, going ahead.

Stock is available at about 9.3x FY14 estimates

Kotak’s 7 Diwali Stock Picks

[download id=”333″]

Cairn India can also be bought as a good ‘future’ dividend stock as it has come out with its maiden dividend and dividend policy which will pay close to 20% of its annual profits as dividend. Readers can read the analysis at http://www.stableinvestor.com/2012/11/cairn-india-dividend-stock-buy-long-term.html