The champion’s rally continues

NIFTY has given 4.3% returns in last 1 month as markets celebrated installation of new NDA govt and win in T20 world cup. Markets are currently consolidating and are sweetly poised given 1) Monsoons have tuned normal last week which is likely to tame inflation and boost rural demand 2) commodity prices are range bound with limited scope of an upward movement in near term and 3) rising hopes of interest rate cuts in later part of the year. Markets are looking forward to first budget of Modi 3.0 in an environment of strong economy and fiscal condition, Rs2.1trln RBI dividend cushion and normal monsoons. We expect renewed focus of GOI on Infra and capex, Rural and Bottom end focus and some concessions to tax paying class, which might provide further boost to economy.

Global geopolitical situation remains a concern as elections outcome in major economies like France, UK, etc. add to uncertainty ahead of US elections in Nov24. We believe Capital Goods, Infra, Logistics/ Ports, EMS, Hospitals, Tourism, Auto, New Energy, E-com and Telecom are potent themes to play, although one needs to be cognizant of valuations. We believe normal monsoons and some concessions for rural and middle class will revive demand in sectors like FMCG, Durables, and Auto, retail and building materials. We increase our base case NIFTY target to 26398 (25816 earlier). We expect market consolidation and recommend buying during market dips.

NIFTY is currently trading at 18.5x 1-year forward EPS, which is at 3.6% discount to 15-year average of 19.2x. Base Case: we value NIFTY at 3% discount to 15-year average PE (18.6x) with March26 EPS of 1417 and arrive at 12-month target of 26398 (25816 earlier). Bull Case: we value NIFTY at 5% premium to 15-year average PE 20x and arrive at bull case target of 28575 (27102 earlier). Bear case: Nifty can trade at 10% discount to LPA with a target of 24493 (23235 earlier).

Model Portfolio: We cut weights HDFC Bank, Kotak, Cipla, and remove BAF and JSPL from model portfolio. We increase weight behind ITC, Titan, Axis Bank, HDFC AMC and Ambuja Cement. We are overweight on cement, Auto, consumer, Capital Goods, Healthcare, Telecom and RIL.

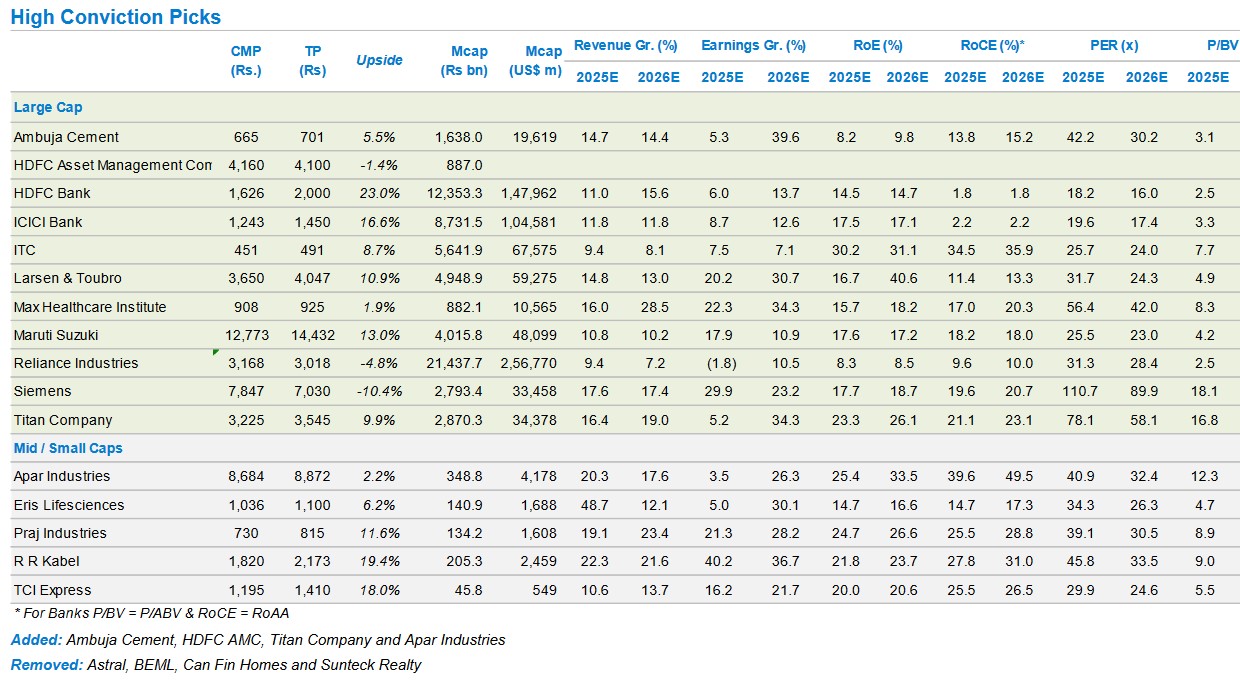

High Conviction Picks: We are adding Ambuja cement, Titan Company, Apar Inds and HDFC AMC. We are removing Suntek Realty, BEML, Canfin and Astral post recent run up in stock prices.

PL Model Portfolio has outperformed NIFTY by 25.8% since Nov 2018, 10.6%

since April 23 and 0.2% since last report.

Conviction Picks Changes

High Conviction Picks: We are removing BEML, Astral, and Canfin as they have already reached our target prices. We remain positive on BEML given strong inflows from Metros, railways and defence; however, the stock has seen a sharp run up in past few months. Astral remains a compelling play on expected growth in housing and construction; however, valuations at 63.5xFY26 leave limited room for re-rating.