Low double-digit revenue growth likely

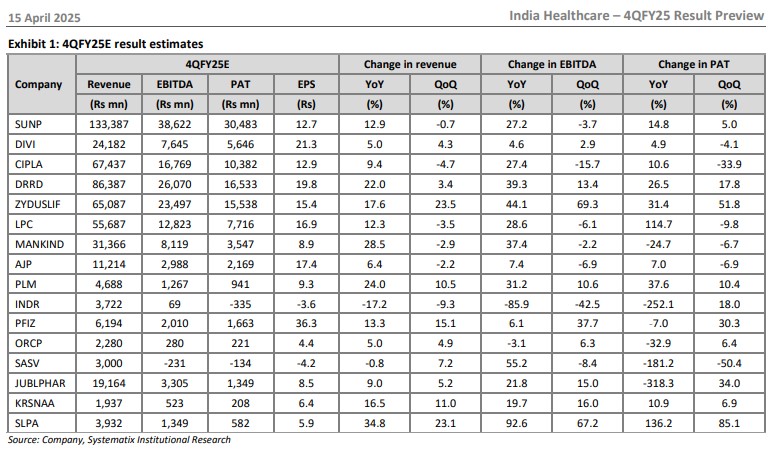

We expect stocks within our pharmaceutical universe to report low double-digit YoY revenue growth (~10%) during 4QFY25. Seasonal weakness in the domestic business could cause a QoQ slow down. We expect select companies in the US to benefit from the ramp up in generic Revlimid [Zydus Life (ZYDUSLIF IN) and Sun Pharmaceuticals (SUNP IN)]. While Cipla (CIPLA IN) may benefit from a revival in generic lanreotide sales (supply issues getting sorted), Lupin (LPC IN) may see a gain in its US portfolio from seasonality (flu and antibiotics). The domestic branded formulation segment should expand in high single digits YoY. Dr. Reddy’s (DRRD IN; led by inorganic initiatives), SUNP, Mankind (MANKIND IN; led by inorganic initiatives) and Ajanta Pharma (AJP IN) may record faster growth than peers. Although there have been no large, meaningful launches in the US during the quarter, we believe ramp up in existing ones would continue to support growth in the US business during the quarter.

1. SUNP – Domestic growth to sustain, while generic Revlimid to support US generics: We expect the contribution from generic Revlimid to step up QoQ and support the company’s US generics business during 4QFY25. On the domestic front, the company may outpace peers to record double-digit growth. From a 4Q earnings call perspective, we expect focus to be on potential growth in its specialty asset – Leqselvi, which is expected to be launched shortly. We estimate -1%/-4%/5% QoQ and 13%/27%/15% YoY revenue/EBITDA/PAT for SUNP, respectively for the quarter.

2. Divi’s Laboratories (DIVI IN) – CRAMS growth could potentially soften, led by upcoming patent expiry: We see CRAMS (expand) growth softening in 4QFY25 due to the upcoming patent expiry of a drug that the company supplies to an innovator. The drug is potentially the single-largest product in DIVI’s base Two key monitorables for the company include a) Timeline of commercial supply for GLP-1 intermediate in its CRAMS business, and b) ramp up in its contrast media portfolio. We estimate revenue/EBITDA/PAT growth of -4%/3%/-4% QoQ and 5%/5%/5% YoY, respectively, for DIVI.

3. CIPLA – US could surprise on Lanreotide recovery and Revlimid ramp up: Supply constraints in generic lanreotide slowed CIPLA’s US business in 3QFY25, but we expect a recovery here in 4Q. Domestic busness could expand in the high single digit-low-double digit range. Timelines for launch of generic Abraxane (recently approved by USFDA), status of generic Advair and potential opportunity from its 505 (b)(2) approval – Nilotinib – would be key focus areas in the quarterly earnings call. We estimate -5%/-16%/-34% QoQ and 9%/27%/11% YoY growth in revenue/EBITDA/PAT for CIPLA, respectively, during 4QFY25.

4. DRRD – US chould revive post weakness in 3Q: Ramp up in generic Revlimid could revive DRRD’s US business in 4Q, post weakness in the 3QFY25. We expect the domestic busines to clock in growth in high teens, led by various inroganic initiatives during the year ( inlicensing of Sanofi Healthcare vaccine portfolio). Cost rationalization, GLP-1 opportunity, Rituximab biosimilar and high value launches in the US would be key focus areas during the quarterly earnings call. We expect 3%/13%/18% QoQ and 22%/39%/26% YoY growth in revenue/EBITDA/PAT for DRRD, respectively, during 4Q.

5. ZYDUSLIF – Sharp sequential growth in the US geography and consumer segment: This could be an extraordinary quarter for ZYDUSLIF, led by sharp QoQ growth in the US, supported by favorable seasonlity in the consumer business. The domestic busienss though could be lackuster. Likely discussion areas in the earnings call: a) follow up on high-value launches in the US, b) timelines around clinical data on Saroglitazar in primary biliary cholangitis, and c) recent acquisition in the medical device space. We estimate 24%/69%/52% QoQ and 18%/44%/31% YoY growth in ZYDUSLIF’s revenue/EBITDA/PAT, respectively, during 4QFY25.

6. LPC – Numbers could be sequentially flattish: US could record mid single-digit growth, led by sesonality and ramp up in high-value products. India business may report high single-digit growth. Tolvaptan launch in the US could be the key discussion area during the earning call, in our view. We estimate -4%/-6%/-10% QoQ and 12%/29%/115% YoY growth in LPC’s revenue/EBITDA/PAT, respectively, during 4QFY25.

7. MANKIND – Exports may weaken QoQ: MANKIND could post strong high-teen growth in the domestic branded prescription formulation business, led by BSV acquisition, which was closed in 3QFY25. We expect the growth revival in its consumer business during 3Q to sustain in 4Q. However, exports may weaken QoQ. Growth acceleration in the domestic branded formulations business and margin expansion would key focus during the quarterly earnings call, we believe. We estimate -3%/-2%/-7% QoQ and 29%/37%/-25% YoY growth in MANKIND’s revenue/EBITDA/PAT, respectively.

8. AJP – Branded markets to grow in double digits, Institutional business may be impacted: AJP may see double-digit YoY growth in its branded markets, led by the expansion in its field force and foray into new therapies. The US business may report flat growth QoQ, given the absence of new launches. Key points that could be discussed during the quarterly earnings call are a) impact on its institutional business owing to the cut in funding, b) expected growth in the US markets in FY26, and c) progress in the branded markets. We estimate -2%/- 7%/-7% QoQ and 6%/7%/7% YoY growth in AJP’s revenue/EBITDA/PAT, respectively, during 4QFY25.

9. Poly Medicure (PLM IN) – Domestic growth slated to strengthen: New launches in the domestic markets and expansion in sales force should strengthen PLM’s 4QFY25 growth, with the export business expected to retain momentum. We estimate 11%/11%/10% QoQ and 24%/31%/38% YoY growth in PLM’s revenue/EBITDA/PAT, respectively, during 4QFY25.

10. Indoco Remedies (INDR IN) – Weakness in the US and elevated expenses persist: Although INDR’s domestic business growth was strong in 3Q, we expect a slowdown in 4Q.We expect the US business to stay weak, as recovery would be contingent on supplies resuming and the company completing the remediation at its sterile facility. The Europe busines could improve QoQ, given the company’s collaboration with Clarity Pharma for the UK markets. Growing debt, USFDA’s reinspection of the sterile facility and acceleration of growth in the domestic / EU markets would be key focus areas of discussion in the quarterly earnings call. We estimate -9%/-43%/18% QoQ and -17%/-86%/-252% YoY growth in INDR’s revenue/EBITDA/PAT respectively, for 4QFY25.

11. Pfizer (PFIZ IN) – Expect growth to rebound: Led by its specialty portfolio – Prevenar, Eliquis and core brands – Becosule, we expect PFIZ’s growth to revive to high single-digit to mid teeens during 4Q. We estimate 15%/38%/30% QoQ and 13%/6%/-7% YoY growth in PFIZ’s revenue/EBITDA/PAT, respectively, during 4QFY25.

12. Orchid Pharma (ORCP IN) – 4Q may see volume-led growth: We believe ORCP would continue to leverage its recently implemented capacities to deliver committed volume growth. However, recent pricing pressures could offset a large part of the same. Pricing improvement, potential new high-value approvals, status of ongoing backward integration project would be the key discussion areas during the earnings call. We estimate 5%/6%/6% QoQ and 5%/-3%/-33% YoY growth in ORCP’s revenue/EBITDA/PAT, respectively, during 4QFY25.

13. Sasta Sundar Ventures (SASV IN) – Retailer Shakti growth momentum to help offset the pain of decline in Flipkart Health: SASV’s Retailer Shakti business will likely continue its strong growth momentum, accentuated by the newly added online business. However, upfront expenses to scale up the online retail pharmacy could dent margins. We estimate 7%/-8%/-50% QoQ and -1%/55%/- 181% YoY growth in SASV’s revenue/EBITDA/PAT, respectively, during 4QFY25.

14. Jubilant Pharmova (JUBLPHAR IN) – Momentum in CRDS and rebound in generic and allergy immunotherapy to shape 4Q performance We expect growth in JUBLPHAR’s CRDS business to continue during the year, given that it has onboarded large innovator clients. The generic business continues to be in the turnaround phase and we could see favorable progress in this space. The allergy immunotherapy business could rebound post some weakness in 3QFY25. While the radiopharma and radiopharmacy?) businesses should deliver high single digit and double-digit growth, respectively, margin contribution will need to be monitored. We estimate 5%/15%/34% QoQ and 9%/22%/-318% YoY growth in JUBLPHAR’s revenue/EBITDA/PAT, respectively, during 4QFY25.

15. Krsnaa Diagnostics (KRSNAA IN) –New center addition to drive growth: We expect KRSNAA to deliver high teens growth during the quarter, which would be led by ramp up in operations at its recently opened centers and addition of new centers. Progress around the B2C intiative and award of new tenders would be key areas of discussion during the quarterly conference call, in our view. We estimate 11%/16%/7% QoQ and 17%/20%/11% YoY growth in KRSNAA’s revenue/EBITDA/PAT, respectively, during 4QFY25.

16. Shilpa Medicare (SLPA IN) – New launches and capacity expansion in the API business to shape growth: Ramp up in generic Nilotinib in the EU market as a sole / first generic and ramp up of 505 (B) (2) launches in the US would shape 4QFY25, in our view. We assume flattish contribution from licensing income, given the uncertainty here. Execution around 505 (B) (2) launches in the US and timelines around new opportunties (transdermal patch, Aflibercept bosimilar, Oxylanthanum carbonate, Nor UDCA, other CDMO opportunities) would be key focus areas during the earnings call. We estimate SLPA’s revenue/EBITDA/PAT to grow at 23%/67%/85% QoQ and 35%/93%/136% YoY, respectively, during 4QFY25.

Review of 16 Pharma stocks with Buy, Hold & Sell recommendations by Systematix Research