The company has taken significant steps to enhance operational efficiencies including improvements in sourcing,...

SMIFS research reports

DIL’s strong brand recall coupled with deeper penetration and consumers shifting towards affordable branded...

Existing hospitals sustained strong performance, delivering a robust 33% YoY revenue growth

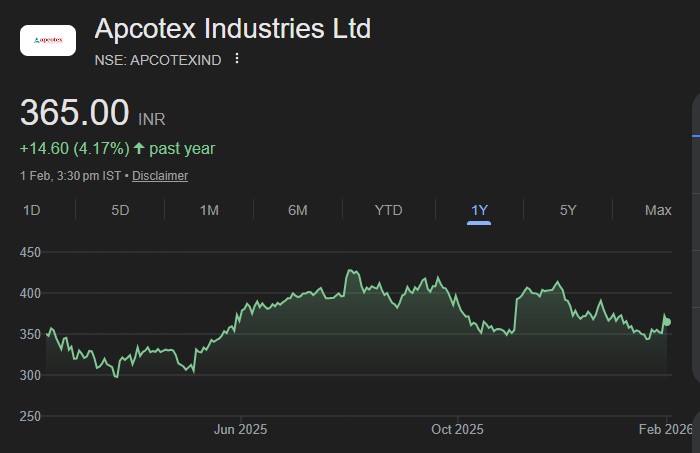

The excitement around recent Anti-dumping duty (ADD) in NBR is waning as finance ministry...

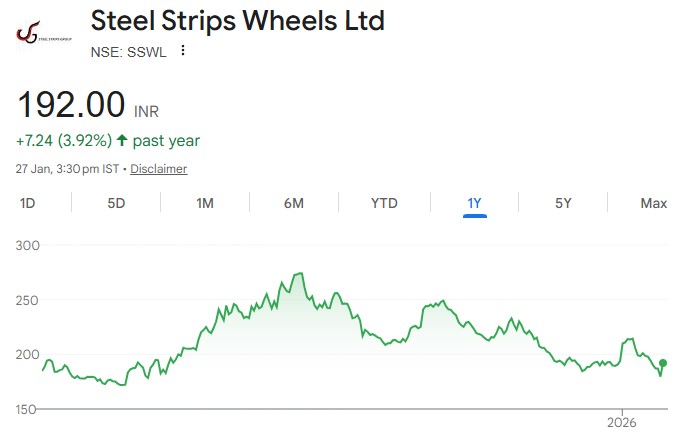

We expect EBITDA per wheel to rise to Rs 264 in FY27E and Rs...

The company has multiple triggers & trading at a steep discount to its large...

Robust performance, Strong growth potential ahead, Maintain BUY! Overall performance was above our expectations....

Decent performance with improvement in textile margin

Robust volume growth & focussing on growth capex are the key triggers.

The current stock price has factored in most of the negatives.