Domestic Economy Shows Resilience; Macro Remains Watchful

The Axis Top Picks Basket delivered a return of 3.2% in Apr’25 against the 3.5% return posted by the Nifty 50, thereby underperforming the Nifty 50 by a slight margin. Over the last one year, the basket has gained 6.8%. Moreover, it gives us immense joy to share that our Top Picks Basket has delivered an impressive return of 310% since its inception (May’20), which stands well above the 163% return delivered by the NIFTY 50 index over the same period.

Domestic concerns addressed; Macroeconomic developments remain a key monitorable: FY26 started with the broad range of twists and turns in the global equity markets led by tariffs imposed by the Trump administration during the first week of Apr’25. The imposition of trade tariffs by the US government on almost all its trading partners has created uncertainty in the global economy, as they are inflationary. These are expected to pose challenges for the US FED in its upcoming policy decisions. The evolution of the ecosystem needs to be closely monitored over the near term. These developments are negative for global growth, and disruptions in the global supply chain could escalate recessionary risks in the US market. Later on, the 90-day pause on the new US reciprocal tariffs provided temporary relief, but it has not eliminated the uncertainty. The 10% uniform tariffs are still in effect, and retaliation from China suggests we are far from a resolution. While India may not be directly impacted, we are seeing ripple effects. Consequently, the second round of impact, driven by the progress in bilateral trade agreements, must be closely monitored in the coming months.

Indian market outperformed in the last one month: Although the challenges for the global economy have increased manifold, Indian equity markets have outperformed the global markets by a significant margin in the last one month. We see several structural reasons for the strong performance, indicating a stronger FY26 than FY25. These are 1) A 50bps CRR cut by the RBI in Dec’24, 2) Consumption boost in the Union Budget, 3) Two rounds of 25bps Rate cuts by the RBI, and 4) Improved liquidity measures by the RBI. These events indicate better days ahead in FY26, with improved credit growth and overall consumption improvements. With all these developments, our benchmark index Nifty-50 went up by 3.5% in the last one month, and the broader market indices, including mid and smallcaps, went up by 4.7% and 1.7% respectively over the same period.

We still believe that at the current juncture, the macroeconomic risks like 1) Trade policy uncertainty related to US and China, 2) Global growth rate (As the US economy saw a contraction in first quarter), 3) The direction of the US 10-year bond yields, 4) The dollar index, and 5) The current geopolitical tension between Indian and neighbouring country will continue to challenge the market direction and market multiple in near term. Keeping this in mind, we believe the market needs to sail through another couple of months smoothly before entering into a concrete direction of growth. As a result, we expect near-term consolidation in the market, with breadth likely to remain narrow in the immediate term. Hence, our focus will remain on style and sector rotation along with earnings recovery. Going forward, we continue to believe that the positioning in the Indian market will likely be divided between the domestic-facing and export-facing sectors. We further believe that at the current juncture, the risk-reward balance favours domestic-facing sectors due to the nil to low impact of the reciprocal tax. Export-oriented sectors will be in a wait-and-watch mode, and the impact and development related to the reciprocal tax will be closely tracked.

The valuations appear attractive for the Largecaps vs. the broader market, where the margin of safety is still missing. Against this backdrop, we believe that the Largecap stocks, ‘quality’ stocks, monopolies, market leaders in their respective domains, and domestically-focused sectors and stocks may outperform the market in the near term. Based on the current developments, we 1) Continue to like and overweight Largecap private banks, Telecom, Consumption, Hospitals, and Interestrate proxies, 2) Are upgrading certain play in retail consumption and FMCG based on the expectation of the recovery in FY26, 3) Prefer certain capex-oriented plays that look attractive at the current juncture following the recent price correction and growth visibility in the domestic market for FY26, 4) Continue to maintain our underweight stance in the IT sector, as we foresee a slowdown in overall IT spending in the US market, and a probable delay in discretionary spending which may pose a downgrade risk in upcoming quarters.

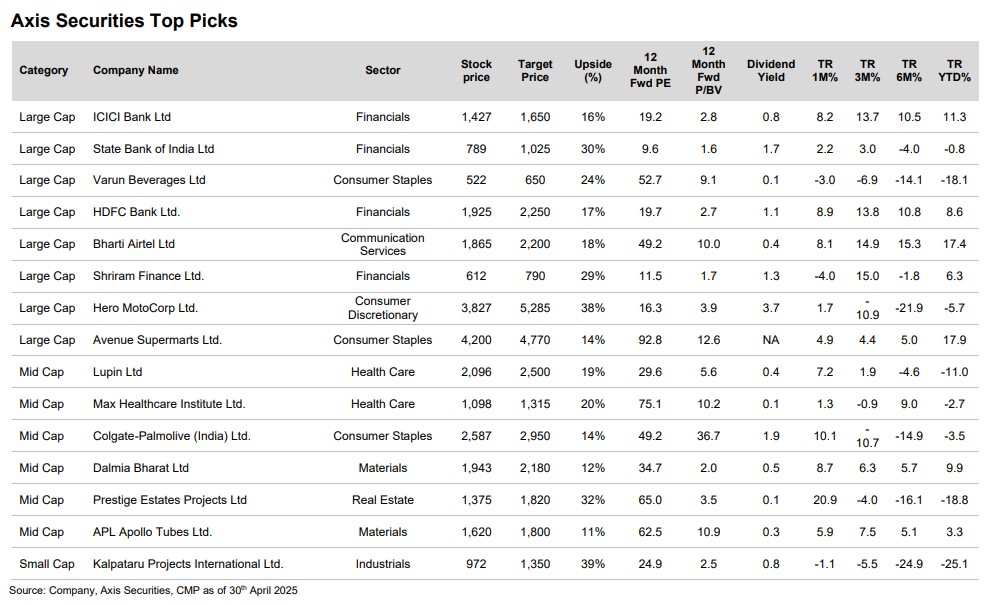

Based on the recent developments, we have made multiple changes to our Top Picks recommendations. This includes the removal of Cholamandalam Investment, Trent, and Indian Hotels, and the addition of Shriram Finance (reasonable valuation after the recent correction), Avenue Supermarts (Expectation of healthier recovery in Value Retail in the second half), and Colgate (Valuation comfort play in FMCG). Our modifications reflect the changing market style and a slight shift towards consumption and domestically oriented play.

Based on the above themes, we recommend the following stocks: HDFC Bank, ICICI Bank, Shriram Finance, Avenue Supermarts, Dalmia Bharat, State Bank of India, Lupin, Hero Motocorp, Max Healthcare, Colgate, Kalpataru Projects, APL Apollo Tubes, Varun Beverages, Bharti Airtel, Prestige Estates