Recent developments indicate that investors Vanaja Sundar Iyer and Siddharth Iyer have acquired stakes of 1.59% and 1.28% respectively in Anondita Medicare, signaling rising interest in this niche SME healthcare player. With a market capitalization of ~₹1,950 crore, the company is gradually gaining visibility among institutional and informed investors.

Business Overview

Anondita Medicare operates in the sexual wellness and healthcare segment, primarily manufacturing male and female condoms. Its flagship brand, “COBRA” condoms, includes multiple variants and caters to both retail and institutional demand.

The company has evolved from a promoter-led business into a listed SME entity, with operations spanning over two decades.

Key highlights of its business model:

- Manufacturing capacity of ~562 million condoms annually

- Strong presence in government tenders and institutional supply chains

- Gradual shift towards own-brand distribution (COBRA)

- Expansion into female condoms and allied healthcare products

Anondita is often seen as a smaller but aggressive competitor to Cupid Ltd, a well-established player in the same segment.

Industry Tailwinds

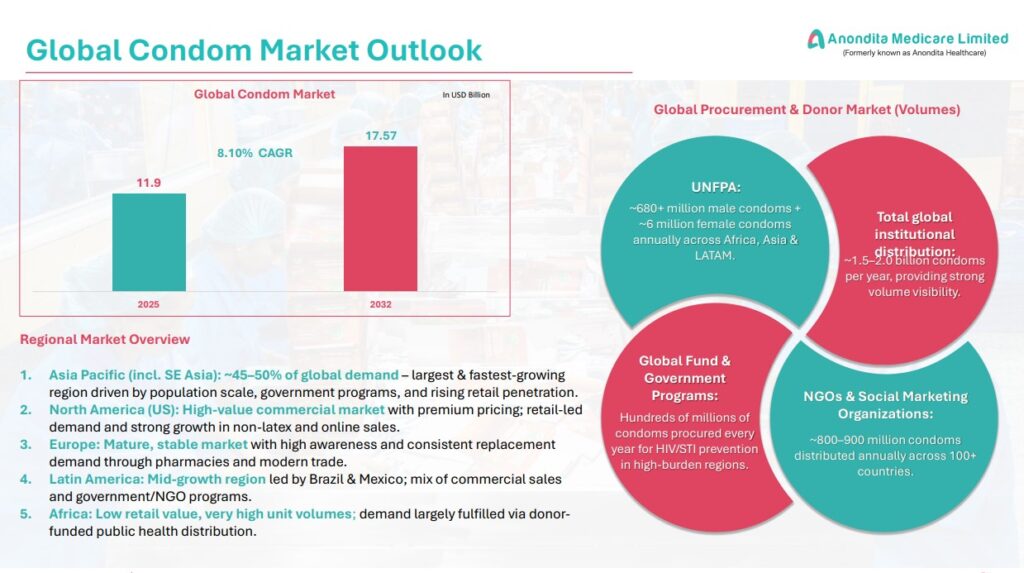

The company operates in a structurally growing market. The global condom market is expected to grow at a CAGR of ~8.1%, reaching ~$17 billion by 2032.

Key drivers:

- Rising awareness of sexual health

- Government-led population control initiatives

- Increased adoption in emerging markets

- Growth of e-commerce and D2C sexual wellness brands

This creates a favorable backdrop for companies like Anondita that combine low-cost manufacturing with scalable distribution.

Shareholding Structure

The ownership pattern reflects a mix of promoter control and institutional participation:

- Promoters: ~62%

- Sageone PMS: ~4.67%

- FIIs: ~3.4%

- New investors:

- Vanaja Sundar Iyer – 1.59%

- Siddharth Iyer – 1.28%

The relatively high promoter holding ensures control, while increasing institutional presence signals improving market confidence.

Financial Performance

Anondita Medicare has shown strong growth in recent years, albeit on a relatively small base.

Revenue Growth

- FY23: ₹35.9 Cr

- FY24: ₹46.4 Cr

- FY25: ₹76.9 Cr

Profit After Tax (PAT)

- FY23: ₹0.35 Cr

- FY24: ₹3.84 Cr

- FY25: ₹16.42 Cr

Key Observations

- Revenue has more than doubled in two years

- Profit growth has been significantly higher than revenue growth, indicating operating leverage

- Margins have expanded sharply

However, such rapid profit expansion may raise questions about sustainability going forward.

Balance Sheet & Cash Flow Insights

- Total borrowing: ~₹27 Cr

- Net worth improving alongside profitability

- Negative operating cash flows in some periods, driven by:

- Rising receivables

- Working capital intensity

- Continued capital expenditure leading to negative investing cash flows

This suggests a growth-stage company, but with execution and cash flow risks.

Strengths

- Cost-efficient manufacturing model

- Strong presence in government and institutional supply

- Growing brand visibility via COBRA condoms

- High return ratios (RONW ~38%)

- Beneficiary of structural industry growth

Key Risks

- Customer concentration risk

- Top clients contribute a significant share of revenue

- Geographical concentration

- Revenue skewed toward limited regions

- Dependence on government tenders

- Exposure to regulatory and policy risks

- Cash flow concerns

- Profitability not fully translating into cash

- Limited listed track record

- Competitive pressure from established players like Cupid

Valuation Perspective

- Estimated P/E range: ~11–16x at earlier stages

- Compared to larger peers like Cupid, valuations appear:

- Lower, reflecting early-stage scale, or

- Discounted due to higher perceived risks

Given its SME nature, valuations may remain volatile and sentiment-driven.

Conclusion

Anondita Medicare represents a high-growth, high-risk SME opportunity in a niche but expanding industry. The entry of investors like Vanaja Sundar Iyer and Siddharth Iyer adds credibility and signals emerging investor interest.

Investment thesis in brief:

- Strong growth supported by sector tailwinds

- Rapid improvement in profitability

- Concerns around cash flow quality and concentration risks

If the company successfully transitions from a tender-driven model to a brand-driven strategy, it could evolve into a meaningful challenger to established players in the sexual wellness space.