Porinju Veliyath’s PMS crumpled from giving an impressive return of 45% CAGR over 5...

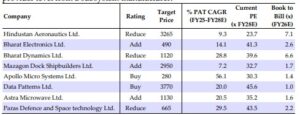

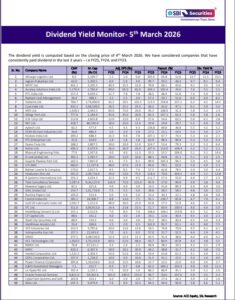

Top Picks

The performance detail of Mohnish Pabrai’s portfolio in the first half of 2018 is...

Raamdeo Agrawal has provided a masterful tutorial about the difference between “quotational loss” and...

Basant Maheshwari’s PMS Fund has clocked in an impressive performance despite the gloomy state...

Dolly Khanna has gone on a buying spree to take advantage of the savage...

Porinju Veliyath’s appetite for so-called “chor” companies has not abated. Instead, he has bought...

A stock which is headed by a so-called “intelligent fanatic” attracted the crème-de-la-crème of...

Shankar Sharma has offered the soothing advice that the savage correction in the stock...

Mohnish Pabrai has confidently proclaimed that there is “significant mispricing” of Indian stocks compared...

Mohnish Pabrai has the luck of the Devil. He has providentially escaped a crippling...