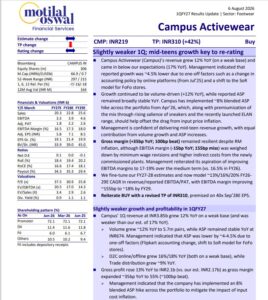

Navigated well in challenging FY26…

About the stock: SBI Life (SBIL) is among the most dominant players in Indian life insurance industry with strong distribution network, parentage, operating metrics.

• Balanced product mix with focus on opex ratio ahead of industry

• Strong parentage led distribution remains key catalyst

Q4FY26 performance: SBI Life delivered steady FY26 performance with NBP growing 20% YoY to ₹42,550 crore, fuelled by strong growth in group savings (₹8,480 crore, +55% YoY), annuity (₹7,030 crore, +34% YoY), and par segment (₹1,670 crore, +123%). While individual savings (₹22,420 crore, +8%) and ULIPs (₹16,500 crore, +2%) showed moderate momentum, protection grew to ₹4,620 crore (+13%) with healthy individual traction (+23%). Despite a rising cost ratio of 10.6% (vs 9.7% YoY) due to GST and labour-code provisions, VNB increased 12% to ₹6,670 crore with margin at 27.5%. Overall, PAT reached ₹2,470 crore (+2%), while balance sheet metrics stayed steady with AUM at ₹4.9 lakh crore (+9% YoY) and solvency at 1.9x.

Investment Rationale

• Focus on favorable product mix and agency channel: Growth outlook remains constructive with management guiding for ~13–14% APE growth over FY27E, supported by consistent execution and more balanced product mix. The company continues to diversify beyond ULIPs, with improving traction in non-par, par and protection, which should support better growth quality as well as profitability. While banca remains the anchor channel with ~60% of APE, regulatory commentary around open architecture has created some overhang on the long-term reliability of exclusive bank-led distribution model. Amidst this backdrop, Management is repositioning the franchise through stronger agency and emerging- channel scale-up, with a gradual 3–4% shift away from banca expected over time. Non-ULIP share in agency improved to ~39% (vs ~34%), aided by stronger traction in protection and savings improving margin profile.

• Margins protected amid regulatory headwinds: VNB margins held steady at 27.5% in FY26 (vs 27.8% in FY25), hitting the upper end of guidance despite absorbing GST-related ITC losses. While an elevated cost ratio of 10.6% (vs 9.7% YoY)—driven by regulatory changes and tech investments—weighs on the structure, management expects a better product mix and higher rider attachment to provide better margin profile. Going ahead, management keeps margin guidance at 26–28% range (internally targeting >27%) through FY27E, balancing growth with profitability, while a healthy 19–20% RoEV continues to drive steady compounding.

Rating and Target Price

• Management’s focus on growth along with product mix, strengthening distribution franchise, is expected to aid margins anticipated within 26– 28% range over medium-term. We value the stock at ~2x FY28E EV, thus continuing with BUY rating with revised target price of ₹ 2200 (₹2300).