Scaling with Strength – Growth, Quality, and FinAI Edge!

Est. Vs. Actual for Q4FY26: NII – INLINE ; PPOP – MISS; PAT – INLINE

Changes in Estimates post Q4FY26 FY27E/FY28E (in %): NII -0.9/-0.9; PPOP -1.5/-0.7; PAT 2.7/1.7

Recommendation Rationale

• Asset quality Entering a Favourable Phase: In Q4, BAF witnessed a sequential improvement in asset quality. Vintage credit performance across 3MOB, 6MOB and 9MOB continues to reflect significant improvement, indicating improved underwriting outcomes. Asset quality improvement would be supported by the winding down of the captive finance book and normalisation in the MSME segment. Resultantly, credit costs are expected to trend downwards and range between 1.45-1.6% in FY26 and are contingent on the gradual easing of geopolitical uncertainties. However, the management indicated that FY27 credit costs guidance includes a certain level of conservatism, considering the macro uncertainty. The management highlighted that ECL provisioning is driven by a bottom-up, product-level assessment done on a quarterly basis, ensuring closer alignment with evolving portfolio risks. BAF has continued to strengthen its PCR across Stage 1/Stage2 reflecting a consciously conservative stance. Importantly, the management indicated a willingness to further build provisioning buffers opportunistically, with the intent of bulletproofing the balance sheet against potential stress events over the medium to long term.

• Broad-Based Growth Momentum with Emerging Segment Driving Growth: In Q4, BAF’s AUM growth was broad-based, albeit temporarily moderated by conscious portfolio recalibration in captive 2-Wheeler financing (expected to be wound down to Rs 1,500 Cr by FY27) and MSME (growth slowed to 6% vs historical range of 20-25%). However, the worst for the MSME portfolio is largely behind, and the management remains confident of resuming double-digit growth in this segment from Q2/Q3FY27 onwards. Incrementally, AUM growth will be driven by newer segments – CV, Tractors and Gold. The newer segment contributed to ~3.5% of AUM growth in FY26 and is expected to scale further on a favourable base. The Gold portfolio is expected to cotninue ot strong growth momentum, supported by doubling the distribution network for gold loans, and is expected to contribute ~5% of the portfolio mix vs ~3.5% presently. At a systemic level, BAF continues to gain share, with ~25bps market share improvement for every Rs 1 Tn AUM accretion, underscoring its ability to grow nearly 2x of the industry. BAF intends to maintain a stable portfolio mix, ensuring balanced growth across segments. The management has guided to add 15-17 Mn customers during FY27 and expects AUM growth to remain healthy at 22-24% in FY27, mainly aided by new businesses launched in the last few years.

Sector Outlook: Positive

Company Outlook: BAF is entering a phase of improved growth and earnings, with AUM growth seen at 22-24% underpinned by normalisation in MSME, winding-down of the captive book, continued market share gains (~2x system growth), and strong momentum in emerging segments such as Gold, CV, 2-wheelers and tractors. Asset quality tailwinds, led by captive run-down and calibrated underwriting, are expected to drive credit costs lower. Importantly, the ongoing FINAI transformation creates a multi-year runway for productivity gains and scalability. Profitability is poised to sustain, with operating leverage and AI-led efficiencies driving cost ratios lower. We expect BAF to register a strong AUM/NII/Earnings growth of 24/22/27% CAGR over FY26-28E while delivering an RoA of 4.4-4.5% over the FY27-28E. BAF continues to reinforce its positioning as a high-quality compounding franchise, underpinned by strong execution, healthy sustained growth delivery drivers, and a strong return ratio profile.

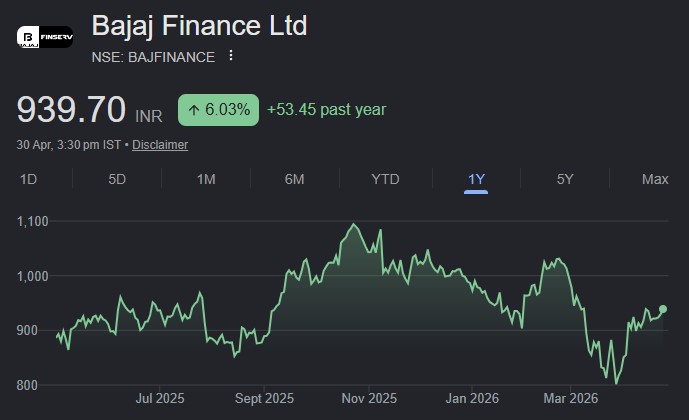

Current Valuation: 4.5x Sep’27E ABV Earlier Valuation: 4.9x Sep’27E ABV

Current TP: Rs 1,160/share. Earlier TP: Rs 1,150/share

Recommendation: We maintain our BUY recommendation on the stock.

Bajaj Finance Ltd – Q4FY26 Result Update – 300426_30-04-2026_10