The Indian healthcare and pharmaceutical sector continues to attract significant institutional attention, and Zydus Lifesciences Ltd. has emerged as a focal point for investors. Global brokerage firm Bernstein recently named Zydus Lifesciences as its top pick in the healthcare space, setting a bullish target price of ₹1,457, which implies a strong 40% upside from its current market levels.

Backed by robust financial metrics, solid ownership, and aggressive shareholder-reward programs, the company exhibits strong fundamentals.

Company Overview & Structure

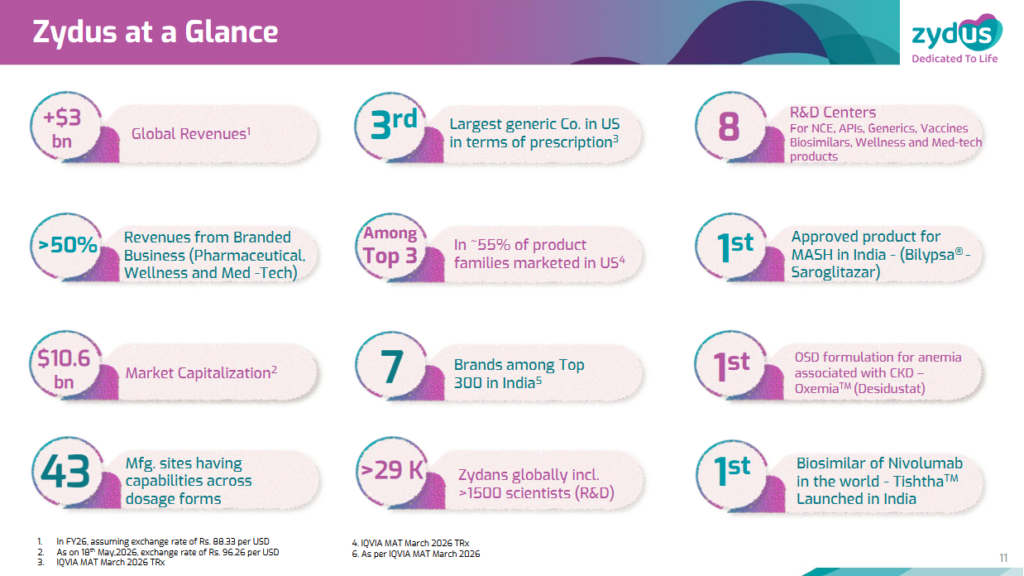

Zydus Lifesciences, headquartered in Ahmedabad, India, is an innovative, global pharmaceutical company that discovers, develops, manufactures, and markets a vast range of healthcare therapies. The company operates across the entire pharmaceutical value chain, including small-molecule generics, biologics, vaccines, and wellness products.

A key pillar of its business structure is its consumer wellness presence. Zydus Lifesciences is the parent company of Zydus Wellness Ltd., holding a commanding 57.59% stake in the entity. This relationship gives Zydus a diversified footprint, combining high-growth pharmaceutical assets with a resilient consumer portfolio featuring household brands like Sugar Free, Glucon-D, and Nycil.

Shareholding Pattern & Key Metrics

Zydus Lifesciences commands a massive Market Capitalization of ₹104,000 Crore, positioning it as a heavyweight in the Nifty Pharma index. The company’s equity structure indicates immense confidence from its founders alongside deep institutional backing:

-

Promoter Group: Holds a highly stable 75% stake, the maximum threshold allowed for listed public companies in India under SEBI regulations.

-

Domestic Institutional Investors (DIIs): Maintain an 11.2% stake, indicating strong faith from local mutual funds and insurance companies.

-

Foreign Institutional Investors (FIIs): Own 6.95% of the company’s equity, highlighting global interest in the pharma giant’s growth story.

Financial Health & Efficiency

Financially, Zydus operates as a highly efficient engine. The company boasts an impressive Return on Equity (RoE) of 21%, signaling a highly profitable utilization of shareholder funds. This level of return is driven by their robust US generics pipeline, a strong domestic formulation business, and growing margins in specialty healthcare products.

Share Buyback Signals Corporate Strength

Demonstrating strong capital allocation and cash wealth, Zydus Lifesciences is actively executing a share buyback program.

Buyback Price: ₹1,150 per share Premium: Represents a 16% premium over the market price at the time of the announcement.

Corporate buybacks at a premium are generally viewed as a strong vote of confidence by management. It implies that the executive leadership believes the company is undervalued, has ample cash reserves, and is dedicated to improving earnings per share (EPS) by reducing the total equity base.

Investment Summary

With Bernstein highlighting the stock for a 40% target upside to ₹1,457, Zydus Lifesciences sits in a sweet spot. The combination of structural stability (via its 75% promoter holding and 57.59% stake in Zydus Wellness), exceptional operational metrics (21% RoE), and value-accretive corporate actions (the ₹1,150 buyback) makes it a compelling candidate for long-term equity portfolios in the healthcare space.

| Stock Name | Bernstein Rating | Target Price (INR) | Core Growth Driver / Rationale |

|---|---|---|---|

| Zydus Lifesciences | Outperform (Top Pick) | ₹1,457 | Innovation basket to add ~$1Bn with a 25% EBITDA CAGR; wellness business driven by GLP-1 protein demand. |

| Lupin | Outperform | ₹2,707 | Complex injectables adding ~$100M in US revenue; projected to lead global respiratory sales by FY28–29. |

| Sun Pharma | Outperform | ₹2,235 | Consistent EPS growth; innovative medicine to cross $2Bn by FY29; Organon synergies adding $1.5–2Bn. |

| Aurobindo Pharma | Market-Perform | ₹1,498 | Flat earnings growth near-term; China+1 API investments add revenue, but $500M biosimilar investments will gestate post-FY29. |

| Mankind Pharma | Underperform (Non-consensus) | ₹2,057 | Identified as a non-consensus underperform idea based on valuation or localized generic headwinds. |

| Biocon | Underperform (Non-consensus) | Not listed | Identified alongside Mankind Pharma as a non-consensus underperform idea. |

- The Longevity Theme: An AI-driven human desire to “live longer, look fitter, and invest in healthcare”. This shifts demand toward next-generation obesity control, wearables, preventive medicine, and digital healthcare.

- The “Rainmaker” Niches: Bernstein highlights six major biopharma areas that will add $70–75 billion to the industry. These include 505(B)(2) NDAs, orphan indications, metabolic peptides, and cellular therapies like CAR-T.

- Ecosystem Maturity: Gains from agentic AI and a rapidly expanding quality control culture are heavily accelerating India’s local clinical innovation capabilities.