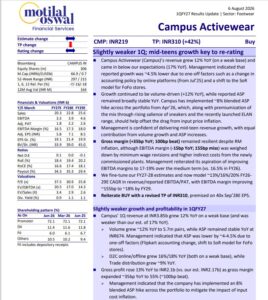

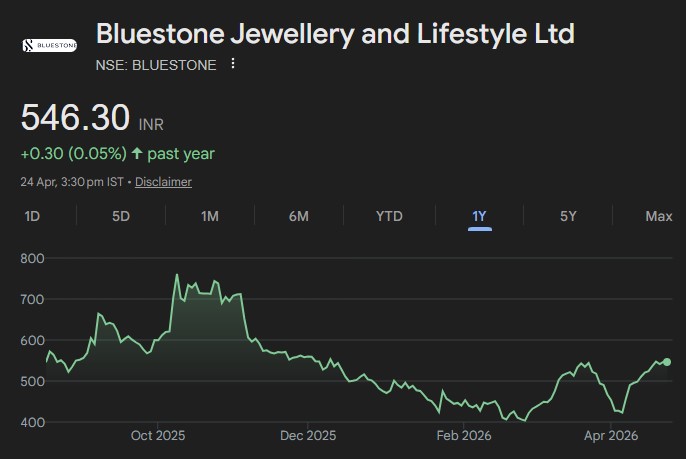

Strong growth, margins normalise sequentially

▪ Strong YoY growth (47.7%). Margin expansion sustains, but QoQ decline signals normalisation from peak levels

▪ Healthy SSSG (~34%) and repeat-led demand underpin growth. Mix and operating leverage remain key to margin trajectory

▪ Maintain BUY on improving operating leverage story; TP raise to Rs 662 per share

Strong YoY margin expansion; sequential normalisation: BLUESTON reported a strong YoY performance with revenue (47.7% YoY / -9.0% QoQ), driven by continued store expansion (23.6% YoY) and healthy SSG (34%). EBITDA margins expanded 1,259 bps YoY to 18.5%, supported by gross margin expansion (520 bps YoY) and lower other expenses (-610 bps YoY). However, margins declined by 376 bps QoQ, reflecting normalisation post a strong Q3 and operating deleverage on sequential revenue moderation. PAT margin stood at 4.6% (1,569 bps YoY) but declined sequentially (-462 bps QoQ) due to lower operating leverage and a continued drag from depreciation and interest costs.

Key Concall KTAs: Q4FY26 commentary indicated steady underlying demand, with SSG of 34% reflecting normalisation post gold price volatility vs any sharp rebound, supported by its design-led portfolio and omni-channel model. Margin expansion remains driven by operating leverage. The company plans to maintain A&P at ~6% of sales, with a gradual shift towards brand-building expenses. Store expansion remains calibrated at ~20% annually, alongside a gradual move away from FOCO. ESOP costs are largely front-loaded and expected to decline from FY27. While inventory remains elevated due to gold price-led MTM impact, underlying efficiency is stable, with normalisation expected. Net debt reduced to Rs 4.85 bn (vs Rs 8.8 bn in FY25), supporting continued expansion. The company reported inventory gain of Rs 509.4 mn in Q4FY26 and Rs 1,805.8 mn in FY26.

Maintain BUY: We believe BLUESTON remains well positioned for sustained growth, on the back of steady underlying demand, improving store cohort maturity, and a scalable omni-channel model. It’s ability to recalibrate product portfolio in response to gold price volatility, along with emerging operating leverage, reinforces confidence in its execution capabilities, although margin stability will remain a key monitorable. We maintain BUY valuing the stock at 25x EV/EBITDA rolling forward to Mar’28EPS with a revised TP of Rs 662 with an upside of 21%.

BluestoneJewelleryandLifestyle-Q4FY26ResultReview24Apr26-Research