We believe HDFCB has managed to outperform large private sector peers previously by effectively...

HDFC Bank

Saurabh Mukherjea has provided valuable advice on how we should construct our portfolios like...

Saurabh Mukherjea has analyzed whether the unending rally in the stock market will continue...

Saurabh Mukherjea has issued the red alert that NBFC and consumption stocks are in...

Goldman Sachs, the leading foreign brokerage which wields strong influence amongst FIIs and HNI...

Saurabh Mukherjea and Raamdeo Agrawal have the same philosophy of investing in stocks with...

Experts have applied their minds and put together a portfolio of top-quality stocks which...

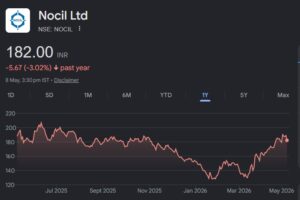

One of Dolly Khanna’s favourite multibagger stocks has come into the limelight after Ashish...

Saurabh Mukherjea has announced that he has dumped a blue-chip FMCG stock which has...

Saurabh Mukherjea has handpicked 4 of the best stocks that we can now buy...