We anticipate healthy double digit net sales growth and operating margin expansion in near...

IDBI Capital

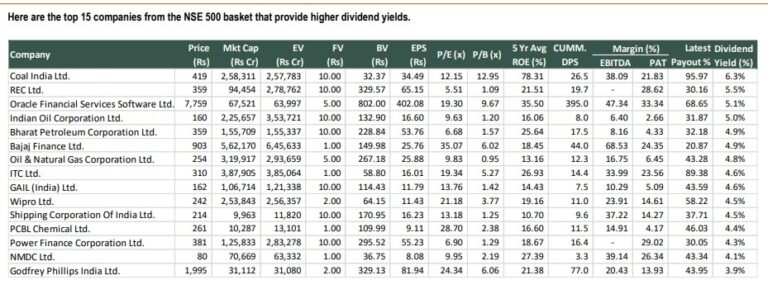

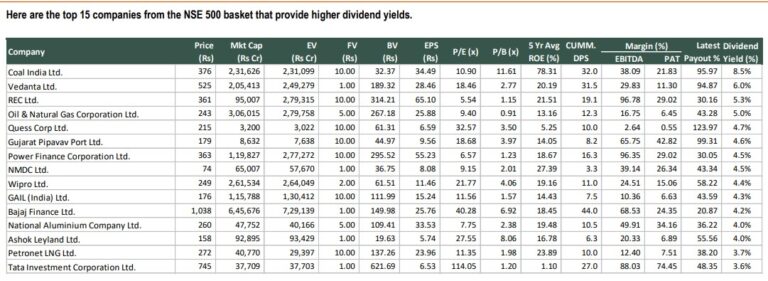

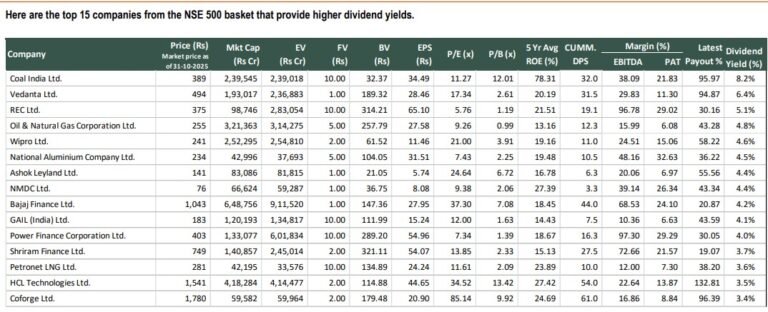

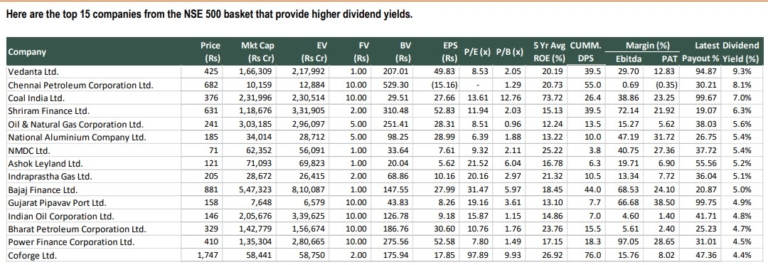

top 15 companies from the NSE 500 basket that provide higher dividend yields

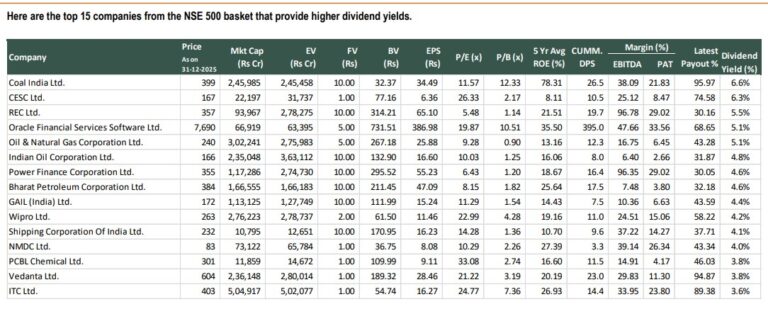

top 15 companies from the NSE 500 basket that provide higher dividend yields

Long-term government contracts provide stable revenue and renewal-dependent cash flows, minimizing volatility and deepening...

List of top 15 companies from the NSE 500 basket that provide higher dividend yields by IDBI Capital

Here are the top 15 companies from the NSE 500 basket that provide higher...

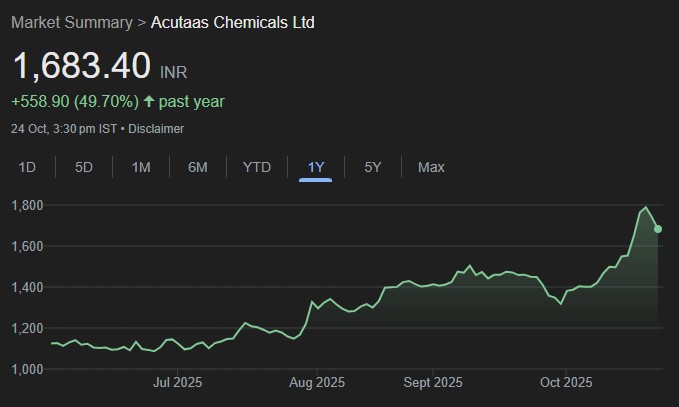

The management is seeing good pick up in electrolytes beginning from Q4FY26 as the...

top 15 companies with high dividend yield

The growth will be propelled

by strong growth in the advanced pharma intermediates business

Here are the top 15 companies from the NSE 500 basket that provide higher...

Cummins India (KKC) delivered robust performance in Q1FY26 which surpassed our estimates. Revenue, EBITDA...